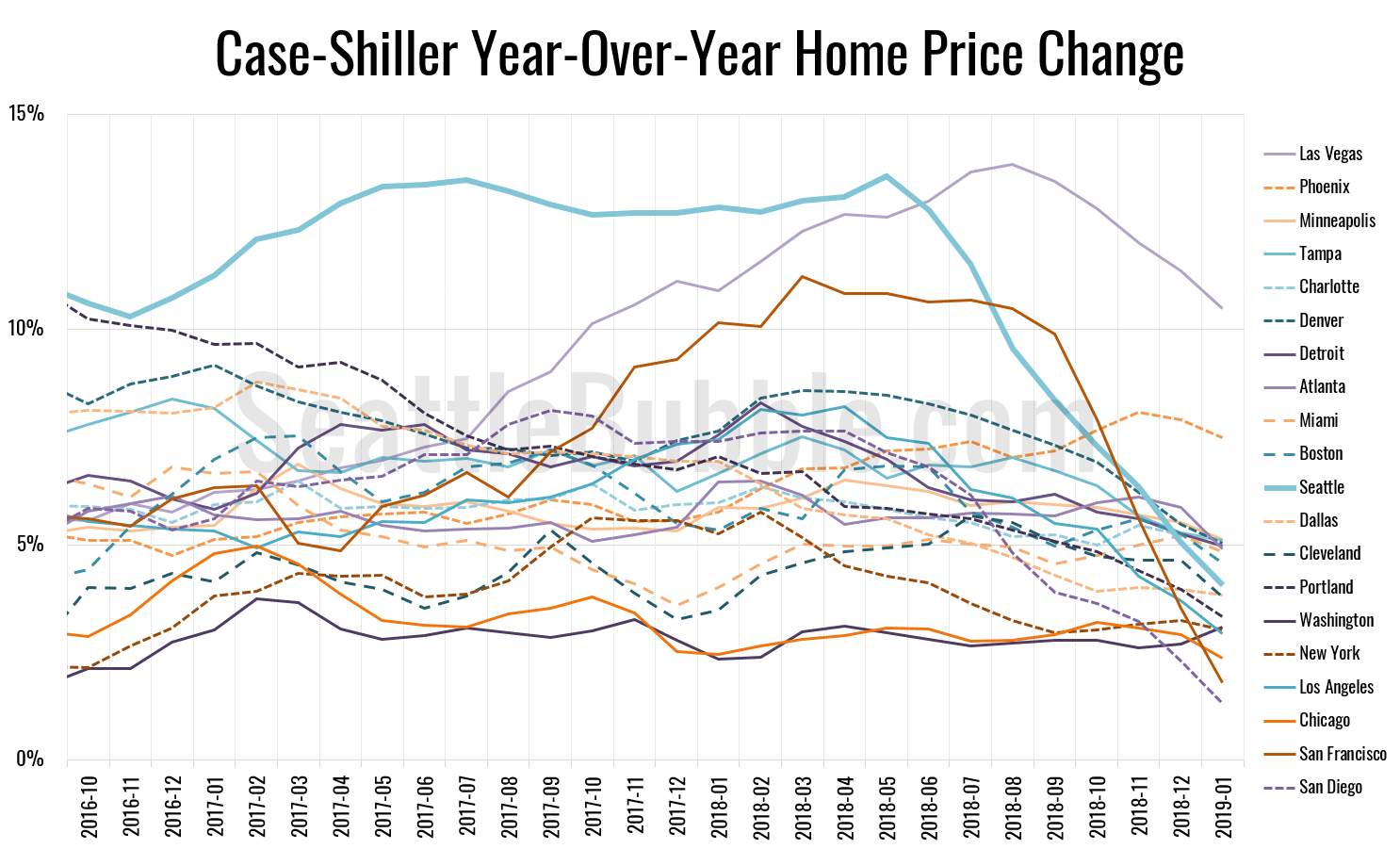

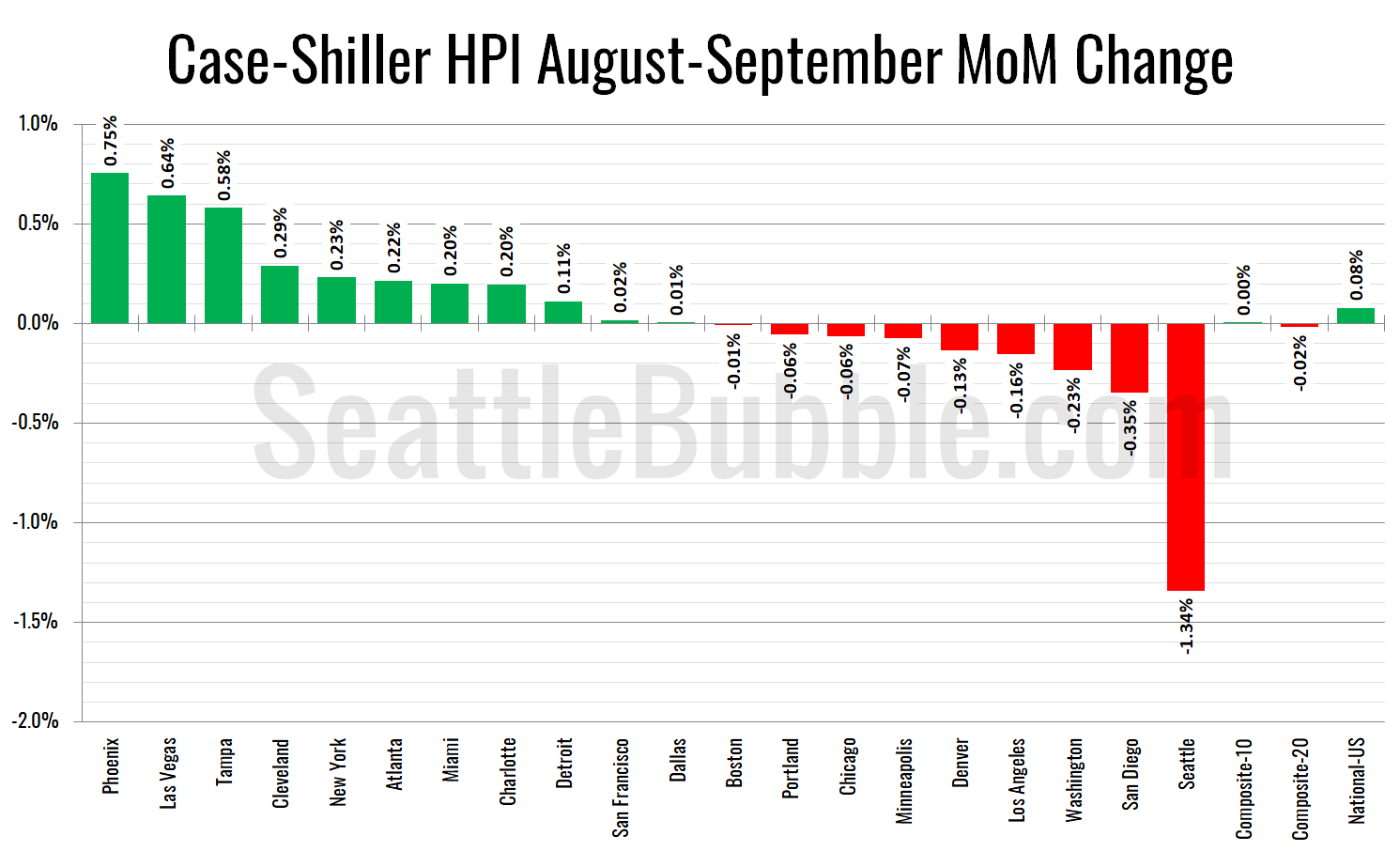

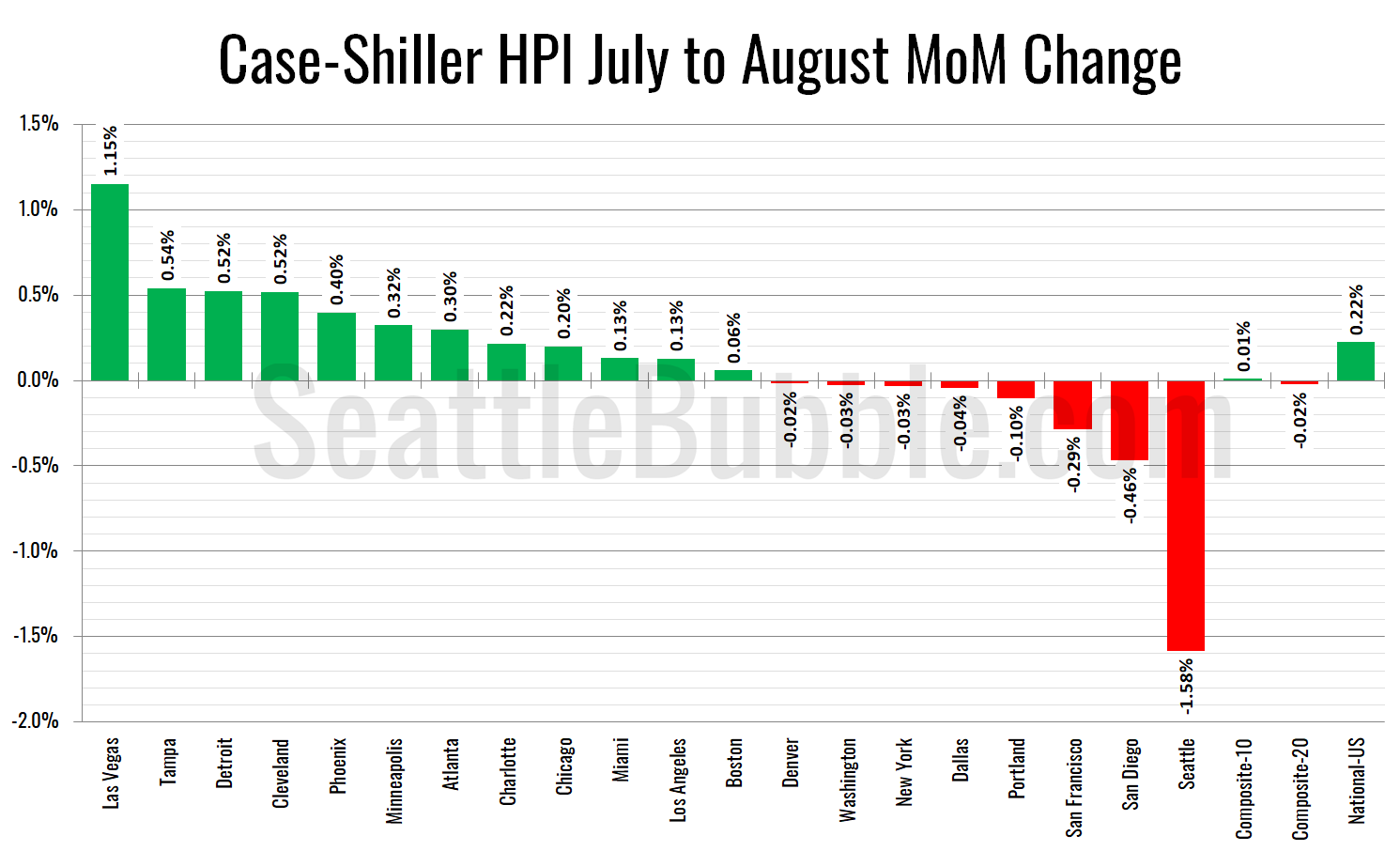

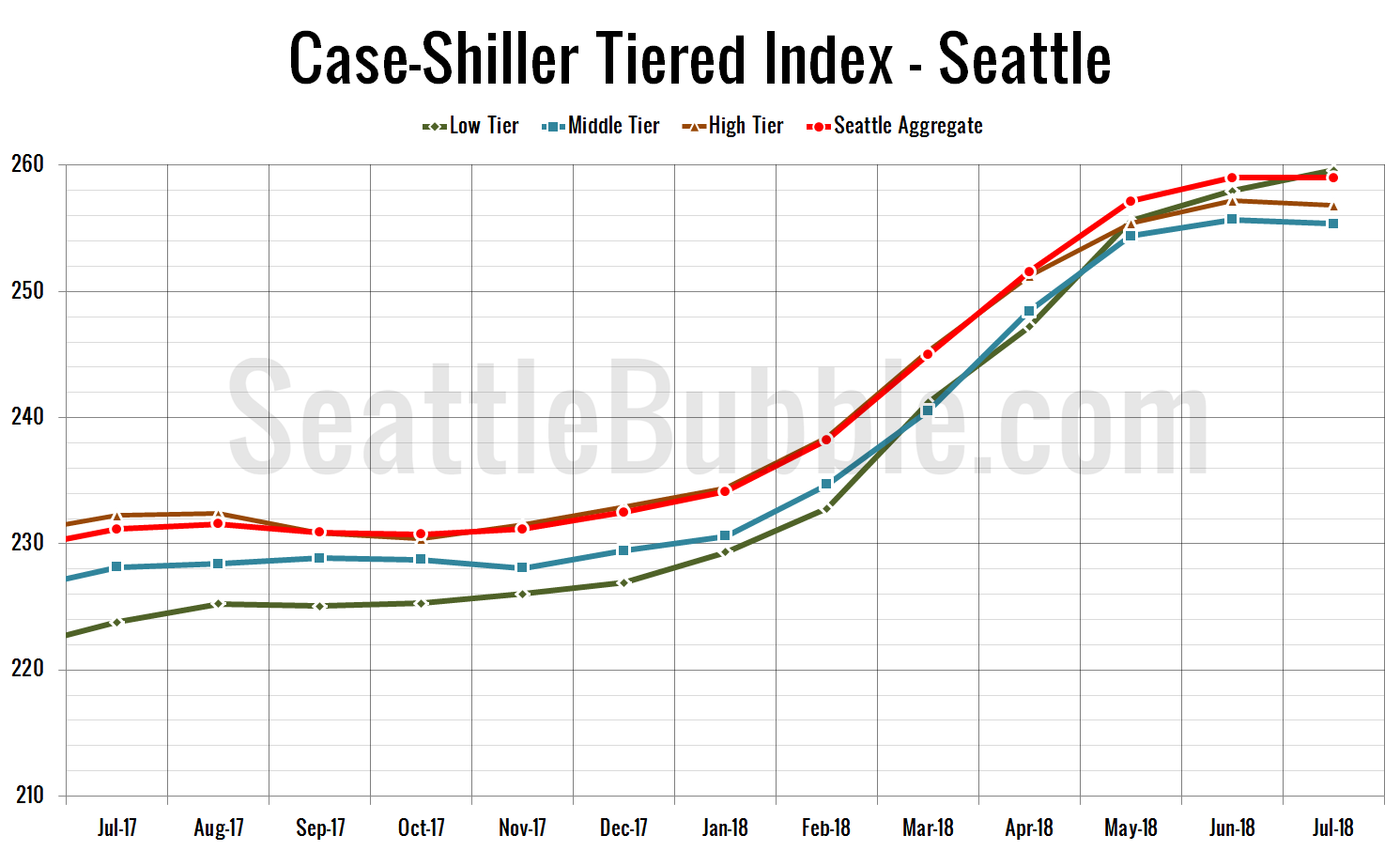

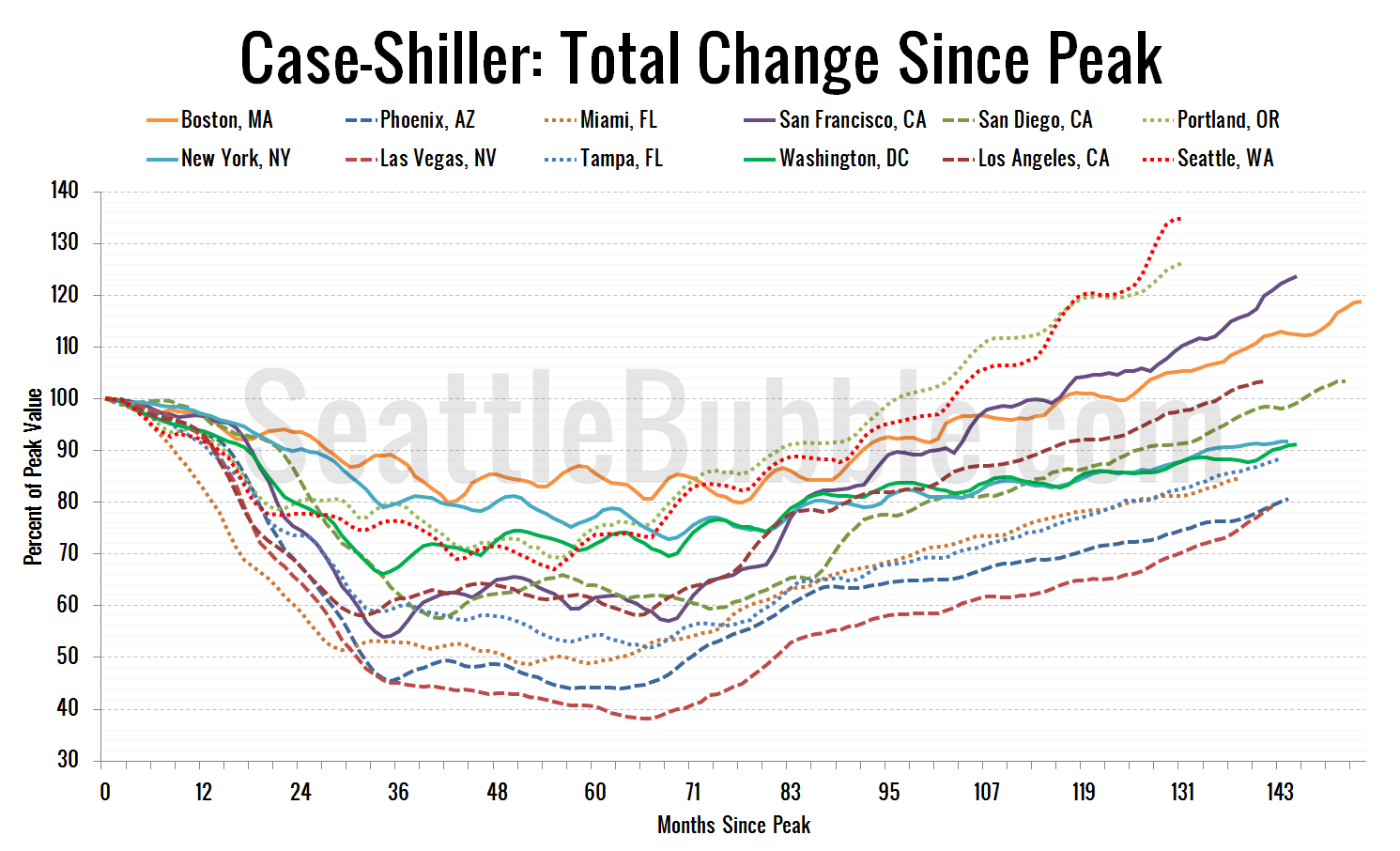

It’s been a while since we posted our Case-Shiller charts and dashboards, so let’s have a look at the latest data from the Case-Shiller Home Price Index. According to January data that was released yesterday, Seattle-area home prices were: Down 0.3 percent December to January…