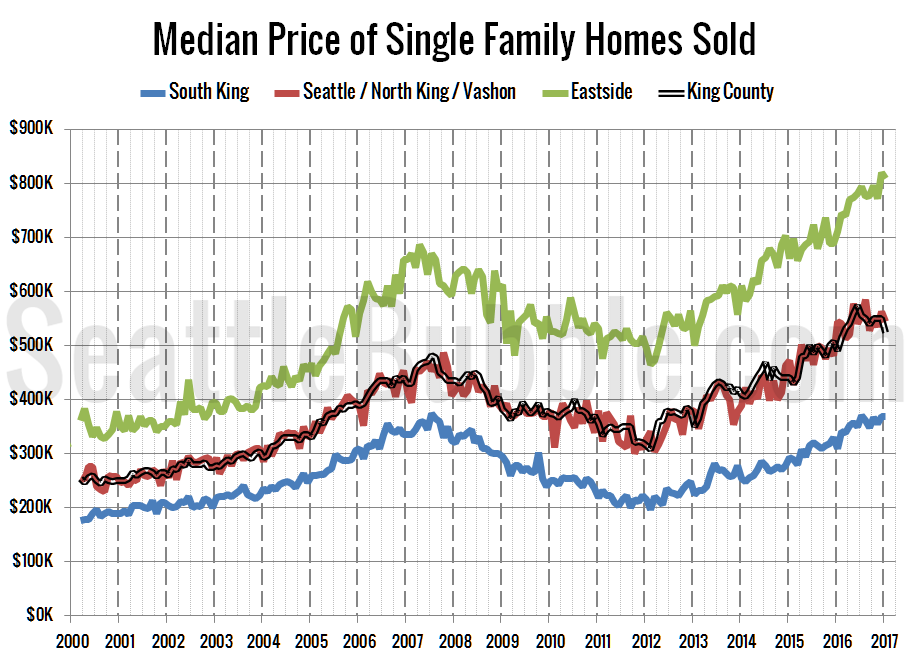

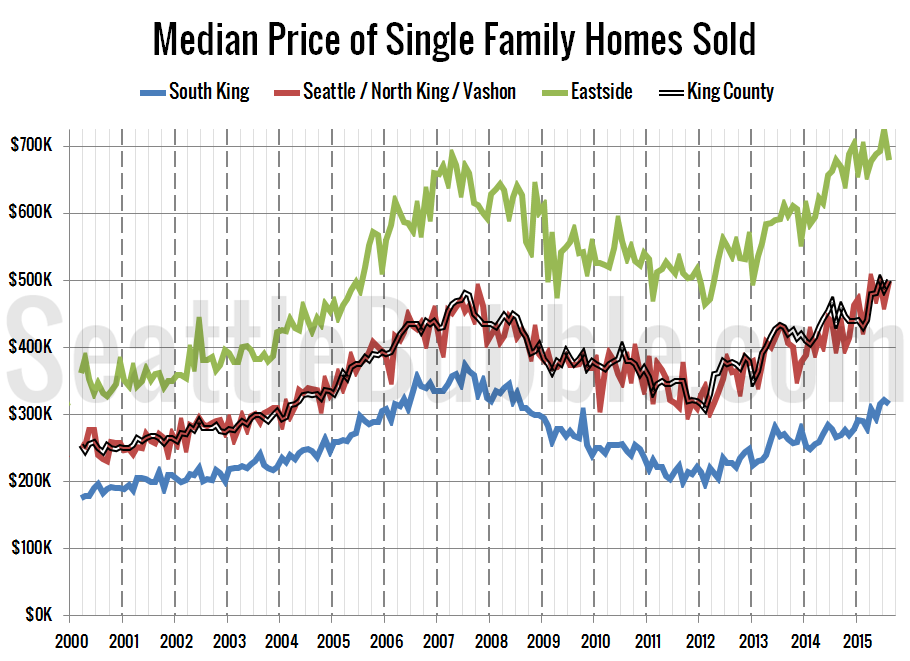

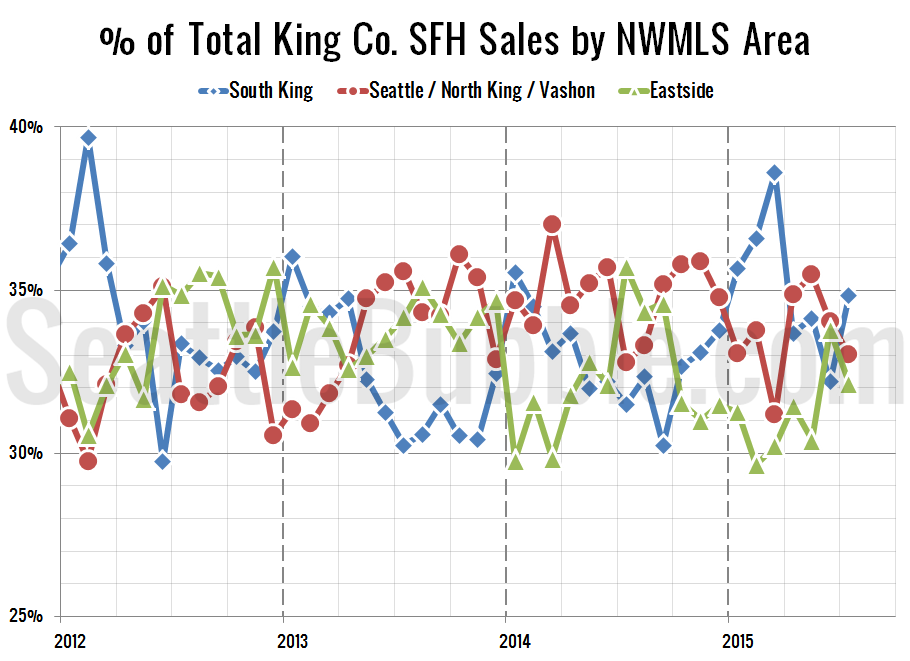

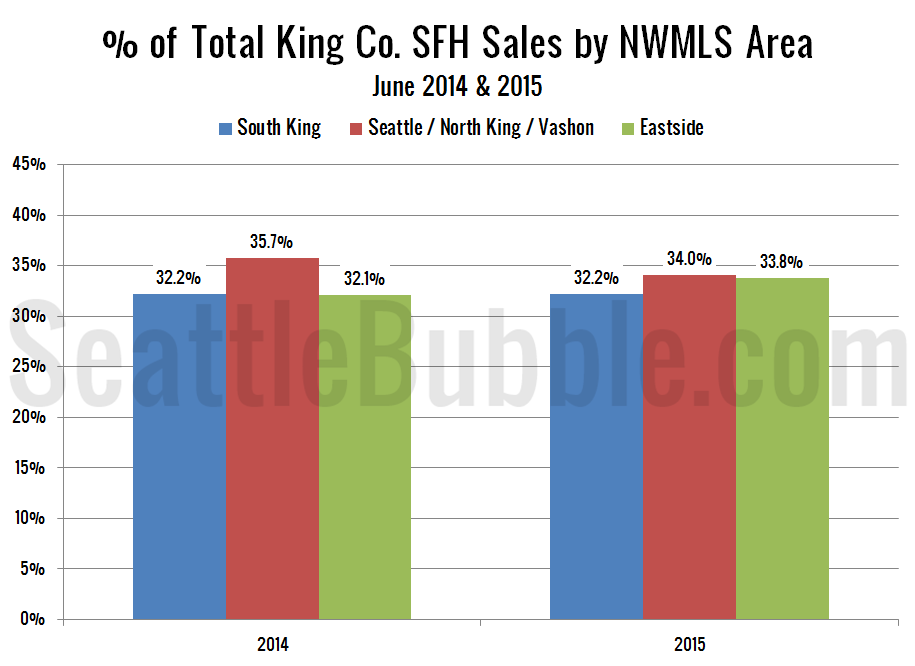

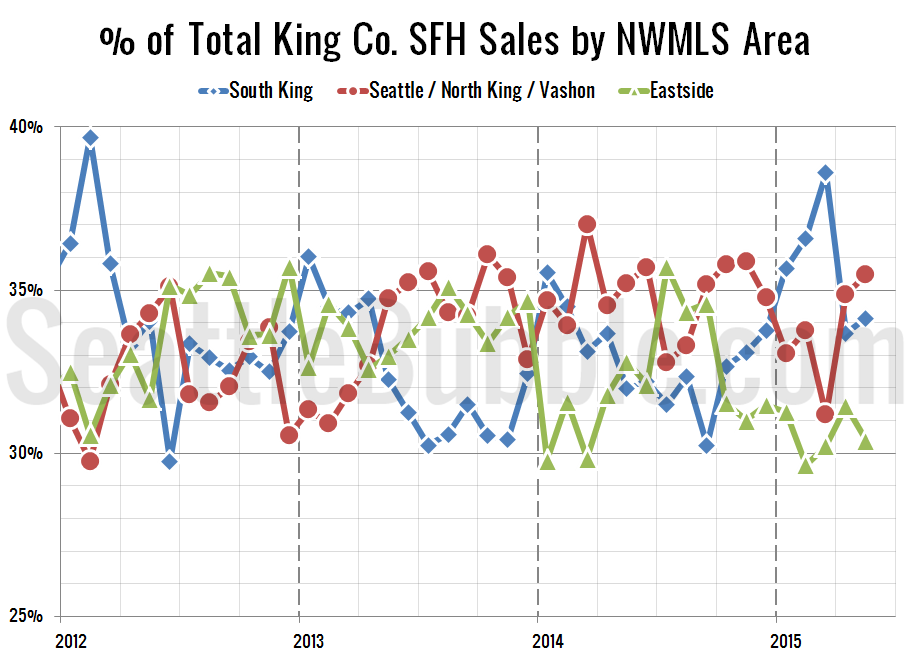

Get unlimited access to the full spreadsheets used to make the charts in this and other posts, and support the ongoing work of this site by becoming a member of Seattle Bubble. It’s been quite a while since we took a look at the in-county breakdown data from the NWMLS to see how the sales…