Let’s check in on the NWMLS statistics from around the sound.

Here’s where the YOY stats stand for each of the six counties as of July 2008:

King – Price: -7.5% | Listings: +22.9% | Sales: -24.4% | MOS: 6.6

Snohomish – Price: -5.5% | Listings: +10.5% | Sales: -32.8% | MOS: 8.4

Pierce – Price: -10.0% | Listings: -5.8% | Sales: -13.2% | MOS: 7.6

Kitsap – Price: -10.9% | Listings: +4.2% | Sales: -15.9% | MOS: 8.9

Thurston – Price: -5.8% | Listings: -6.1% | Sales: -24.8% | MOS: 6.4

Island – Price: -18.8% | Listings: +8.9% | Sales: -13.5% | MOS: 10.7

Skagit – Price: -3.9% | Listings: +8.5% | Sales: -19.2% | MOS: 9.0

Following below are the graphs you’ve come to expect. Click below to continue reading.

These graphs only represent the market action since January 2006. If you want to see the long-term trends, feel free to download the spreadsheet (or in Excel 2003 format) that all of these graphs come from, and adjust the x-axis to your liking. Also included in the spreadsheet is data for Whatcom County, for anyone up north that might be interested.

First up, it’s raw median prices.

Median prices declined from June to July in King, Pierce, Kitsap, and Island counties, and increased in Snohomish, Thurston, and Skagit. The largest drop was in Island, where the median price dropped over $20,000.

Here’s how each of the counties look compared to their peak:

King – Peak: July 2007 | Down 7.5%

Snohomish – Peak: March 2007 | Down 8.5%

Pierce – Peak: August 2007 | Down 10.8%

Kitsap – Peak: September 2007 | Down 12.3%

Thurston – Peak: July 2007 | Down 5.8%

Island – Peak: August 2007 | Down 26.9%

Skagit – Peak: June 2007 | Down 13.7%

Thurston County still holds the prize for smallest total decline, with Island County way out in front for largest decline, rapidly approaching 30% off peak.

Here’s another take on Median Prices, looking at the year-to-year changes over the last two years.

The ever-noisy data for Skagit County bumped back into positive YOY territory last month, with year-over-year price declines elsewhere in the sound ranging from a 5.5% drop in Snohomish to a huge 18.8% drop in Island County.

Here’s the graph of listings for each county, indexed to January 2006.

Listings resumed their increase in every single Puget Sound county in July, with Island County seeing the largest jump and setting a new high point for listings in that county.

Here’s a look at the YOY change in listings.

Thurston and Pierce continued in negative YOY range for listings.

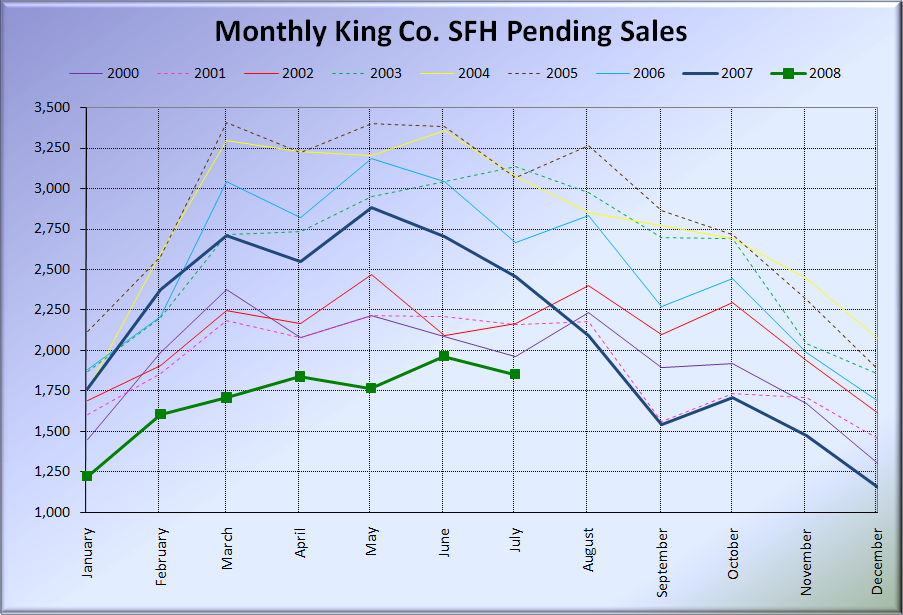

Lastly, let’s check out pending sales, also indexed to January 2006.

Kitsap, Island, and Skagit all broke above the January 2006 sales mark, while King slipped back below. Note that in King County May or June is typically the high point for pending sales (see graph). It seems unlikely that we will break back over the January 2006 sales volume. If I were to describe sales in a word, that word would be anemic.

Lastly, here’s the YOY graph of sales:

{kind=link}

Even the best-performing counties are still seeing sales volumes 13% lower than July last year, while Snohomish continues to pull up the rear with 30% fewer sales. Ouch.

Island County continues to be the big loser as far as prices and “months of supply” are concerned. With record inventory that continues to rapidly build, I suspect prices there will continue to drop for some time.