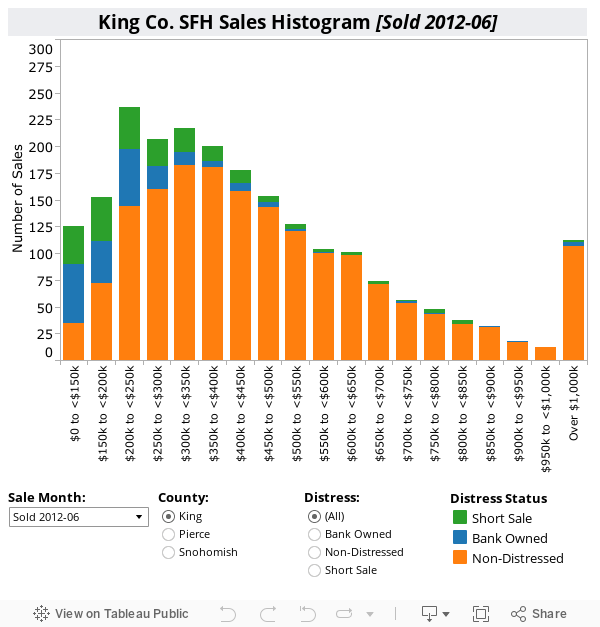

In order to get a little bit better of a feel for how the tax credit expiration is affecting the sales mix, let’s take another look at a histogram of single-family home sales in King County.

To generate the chart below, I downloaded all the sales data for homes sold in King County from the beginning of the year through the end of July. Since my data download puts late-reported sales into the month that the sale actually took place rather than in the month they were reported, there is a slight difference in the number of sales I’m counting vs. what the NWMLS reports each month.

The NWMLS reports showed 1,879 sales in June and 1,474 in July (a 22% MOM drop), while my data includes 2,008 sales in June and 1,425 in July (a 29% MOM drop).

If you flip between June and July, you will see that while home sales dropped steeply in all price tiers between June and July, sales of homes priced $250k to $300k fell the furthest, falling from 292 in June to just 150 in July (a nearly 50% drop).

Considering that the tax credit was primarily available to first-time homebuyers, it makes sense to see the $250k-$300k range take the biggest dive. That’s about at the top of where I would expect most first-time homebuyers to be shopping, and it’s not surprising that the kind of buyers that are persuaded by an $8k check from the government would be buying the most expensive houses they can.

Of course, when you remove a huge chunk of sales from a below-median price bracket, what happens to the median price? It goes up, of course. The median price of the 2,008 June sales I analyzed was $380,000, while the median of the 1,425 sales in July was $389,000. That’s a 2.4% increase in a month (an over 30% yearly rate of increase), but it means absolutely nil about the value of any individual homes.