It’s time once again for a reporting roundup, where you can read my wry commentary about the news instead of subjecting yourself to boring rehashes of the NWMLS press release (or in addition to, if that’s what floats your boat).

…

For a month that saw home prices shoot up to insane new all-time highs, the quotes from home salesmen in this month’s release are surprisingly calm.

I do want to address one glaring error in the release, though:

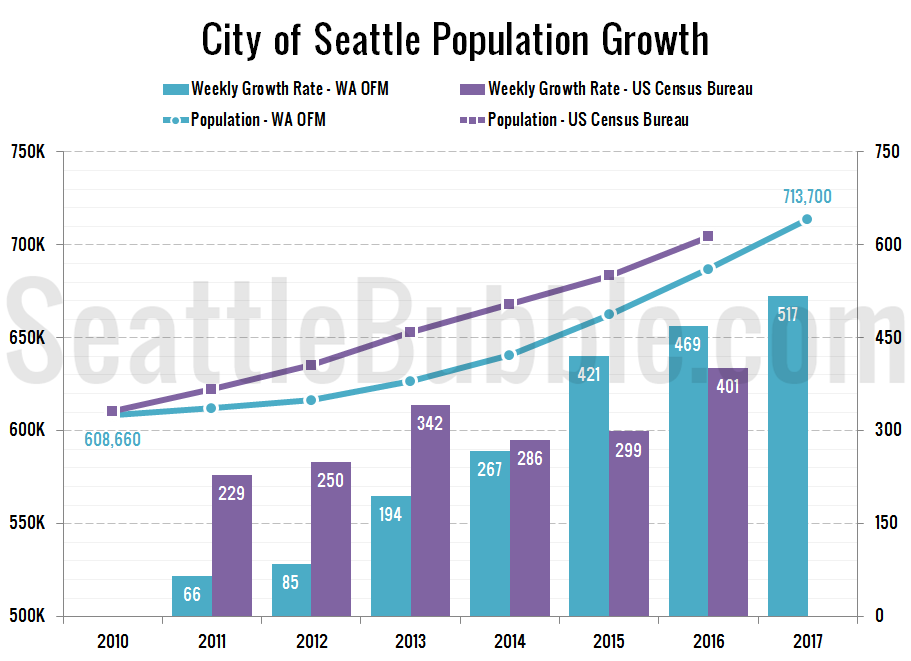

Seattle’s growing population is another likely factor. Recent U.S. Census Bureau data shows Seattle is gaining about 1,100 residents per week, an “astounding” figure, said MLS director Diedre Haines.

That number is false. The most recent data available shows a growth rate of less than half that level…