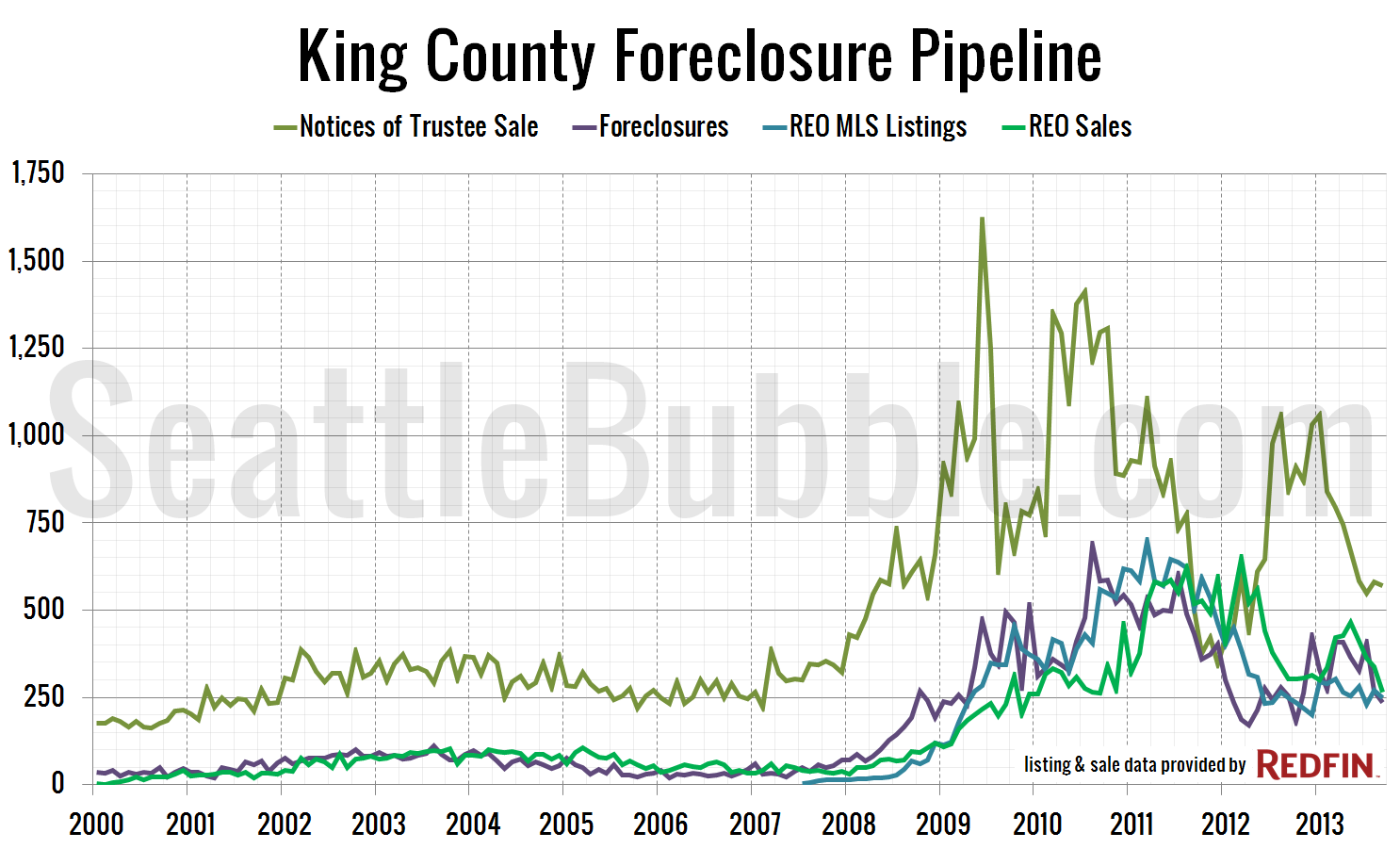

A little over a year ago, I wrote a series of posts in which I argued that “shadow inventory” (foreclosed homes held off the market by the banks) was nearly non-existent. "Shadow Inventory" Conspiracy Theories Are Nonsense Shadow Inventory Gut Feelings, Rumors, & Anecdotes Undocumented Shadow Inventory Scarce in King County Despite all of the…

Tag: banks

Have You Faced Deficiency Judgment?

Have you faced a deficiency judgement on a home you lost to foreclosure? A global cable TV network is looking for Seattle-area borrowers who have been through the process of a deficiency judgment for a story they’re working on. If that’s you and you’re willing to talk about it for a television business show, contact…

Undocumented Shadow Inventory Scarce in King County

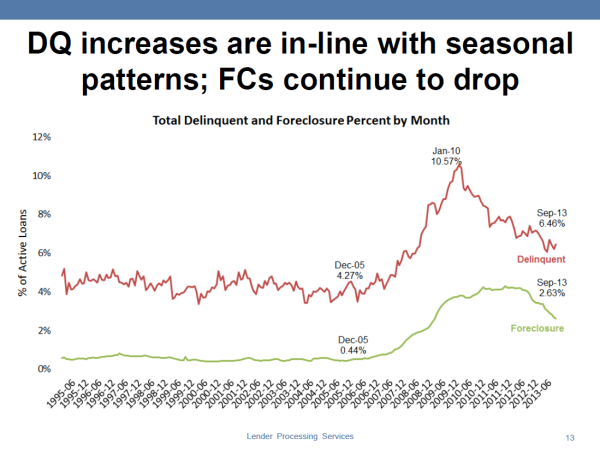

Don’t worry: This will be my last post about the shadow inventory issue for quite some time. In last Friday’s post about shadow inventory, “Haybaler” shared a great link in which Calculated Risk reported LPS delinquency data for September. This data addresses the main complaint some of you have raised about my previous analysis of…

Shadow Inventory Gut Feelings, Rumors, & Anecdotes

A number of you took issue with my data-backed claim that foreclosures are proceeding in a normal, orderly fashion and shadow inventory is a non-issue in the Seattle area. Your main objection seems to be based on a belief that there are large numbers of homes with mortgages that the borrower has stopped paying months…

“Shadow Inventory” Conspiracy Theories Are Nonsense

For some reason, a couple weeks ago the Seattle Times website featured a syndicated article about RealtyTrac’s “Vampire REO” nonsense, which in addition to being a completely worthless bit of non-news, was already weeks old when it appeared on the front page of the Seattle Times website. In the comments to the article I did…