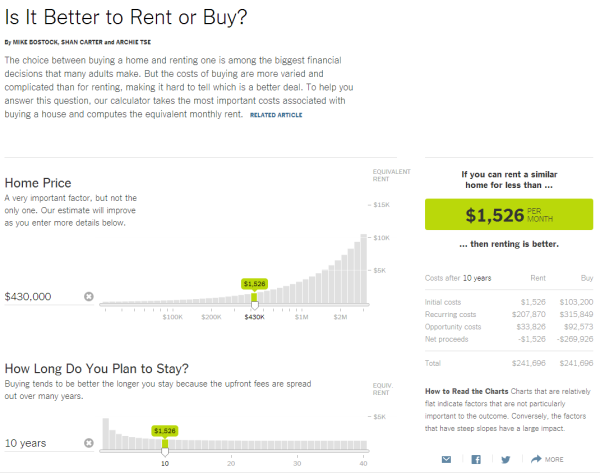

For years, the gold standard in online buy vs. rent calculators has been the one created and hosted by the New York Times. This week, they released a brand new, updated and enhanced version: Is It Better to Rent or Buy? The new version lays out all of the variables in a clean and simple…