A little over a year ago, I wrote a series of posts in which I argued that “shadow inventory” (foreclosed homes held off the market by the banks) was nearly non-existent. "Shadow Inventory" Conspiracy Theories Are Nonsense Shadow Inventory Gut Feelings, Rumors, & Anecdotes Undocumented Shadow Inventory Scarce in King County Despite all of the…

Tag: Redfin

Redfin Gains Instant National Footprint With Acquisition of Walk Score

Full disclosure: The Tim is currently a Redfin shareholder. Well this is interesting. Redfin was one of the last real estate search sites to integrate Walk Score into their listing pages. Today Redfin announced that they have acquired Walk Score. From Redfin’s blog post: The acquisition is Redfin’s first and the reason for it is…

Alternative Brokerage Spotlight: Redfin

Full disclosure: The Tim was employed by Redfin, and is currently a shareholder. Read the series intro: Alternative Brokerages Flourishing Around Seattle First up in our in-depth series on alternative brokerages around Seattle is the technology-powered real estate brokerage Redfin. Redfin was started here in Seattle in 2004, and currently serves buyers and sellers in…

Alternative Brokerages Flourishing Around Seattle

Full disclosure: The Tim was employed by Redfin, and is currently a shareholder. WaLaw Realty and Quill Realty are current advertisers on Seattle Bubble. For some reason, the Seattle area has become home to the cutting edge of real estate. On the technology front, we’re home to Redfin, Estately, Zillow, ActiveRain (a division of Trulia),…

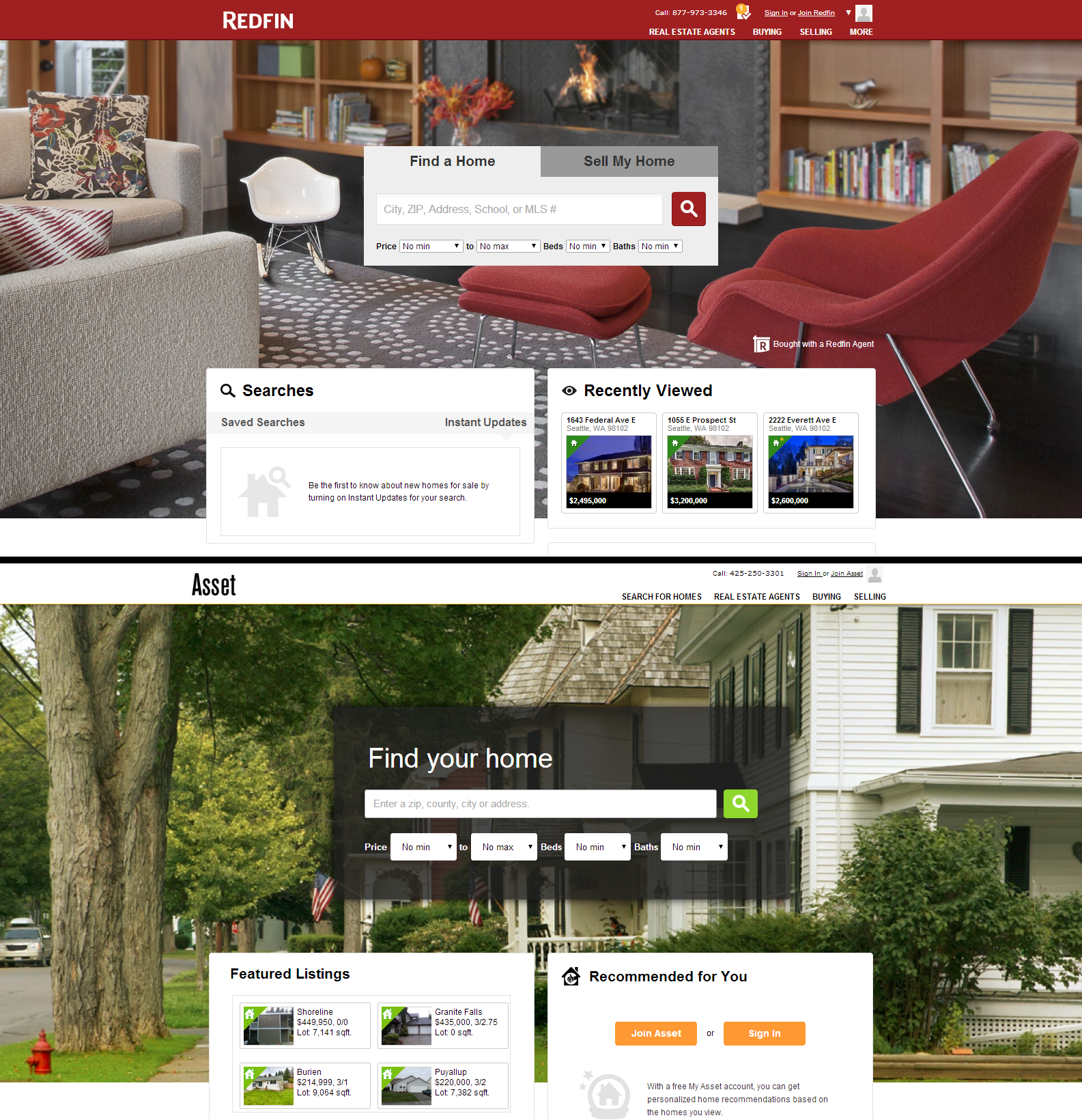

Sleazy Kirkland Brokerage Rips Off Redfin Design & Code

Imitation may be the sincerest form of flattery, but straight up ripping off someone else’s hard work is… something else. The latter describes what Asset Realty Group, a sleazy Kirkland-based brokerage, is clearly guilty of. Let’s take a tour of a shameless rip off, shall we? Home Page The home pages are very similar, but…