Living most of my life in Florida, cockroaches were a fact of life. In general, if you spotted one cockroach, that meant there were at least 1,000 others somewhere, waiting in the wings.

In the past few months homeowner subprime sob stories have been coming at us from all over the country, ad nauseam. With Washington state in the top five for toxic loans, you’d figure we’d see more local stories.

{kind=link}

Here’s one from the Seattle Times this morning: Borrower, beware: Debt disaster looms as rates rise on easy-money mortgages

It was a sweet little house, with affordable day care nearby for their 6-year-old son. Patrick Fultz and Laurel Swartz were hooked.

But when the couple — with no savings and about $20,000 in credit-card debt — shopped for a mortgage to buy their 1,200-square-foot house in Tukwila last year, they heard the same thing from lenders and in a home-buying class they attended: Forget it.

“You basically had to be Scot free, no massive credit debt, which we had, and to have money in the bank, which we didn’t,” said Swartz, 31. “How do people buy houses in America anymore?”

Fultz thought he had found just what he was looking for when he came across Gold Mortgage Lending in Renton on the Internet. “No income verification mortgage, zero down,” read the firm’s Web site. “We fund mortgages the others can’t.”

Erin Rearden, a mortgage counselor at Solid Ground, a nonprofit social-service agency in Seattle, said the deal Fultz and Swartz struck is typical, especially as the cost of housing skyrockets out of reach for so many.

“They wanted a home. And a lot of this comes from operating under the assumption that owning a home is an inherent American right. So when someone offers a way to do it, you want to go for it,” she said.

Fultz makes $12.75 a hour driving a fish-food delivery truck. He recently paid off half of the 12 credit cards he used in buying a motorcycle, a couch and a television, going out to eat, “just buying stuff,” Swartz was working at an insurance office, where she made $11.75 an hour.

The couple signed two mortgages to buy their $246,800 house in July. The first loan, a so-called pick-a-payment loan for 80 percent of the deal, had a variable interest rate. The second mortgage, at 12.5 percent interest, covered the rest.

Not long after they signed the loan, Swartz decided to dump her sedentary office job to become a personal fitness trainer. The new job paid less, $7.89 an hour, but she had the opportunity to earn commissions as she brought in clients.

The commissions, however, didn’t materialize. At the same time, the interest rate on the first mortgage went up, from 7.06 to 8.15 percent — and it can go up every month until topping out at 11.5 percent.

Suddenly the couple were $300 a month short of paying their bills.

“I feel sorry for anyone who can’t get into a house,” Mills said. “We beg the banks to give us their turn downs. I help people; that’s the bottom line.”

Editors note: Always watch your back when a commissioned salesperson beings a sentence with “I help”

But today, people like Fultz and Swartz aren’t the only ones having money problems. Mills, and brokers like her, have troubles of their own.

A meltdown in the subprime lending market is drying up the money pipeline.

Across the country, where home values are stalled or plummeting, lenders are watching loans turn upside down, with mortgages grown larger than property values. People behind in payments are losing their homes. Entire neighborhoods in parts of the Midwest and California are shuttered by bad debt.

The situation is nothing like that in Seattle, where increasing home values can still grease the mechanics of subprime deals.

But even here, lenders have stopped serving subprime clients or are imposing tighter requirements to qualify, from higher credit scores to a couple of months’ worth of payments in the bank and at least some money down.

“For my clients, that is a deal killer,” Mills said. “My clients don’t have any money.”

Wait a minute… I’m confused. I thought your customers were people that already didn’t have any money? Or were you talking about the money to pay your broker fees?

The pullback has cratered the business model for brokers like Mills. She used to write 10 to 15 loans a month. In March, she wrote two. In February? None.

“I didn’t make my own mortgage payment this month,” Mills said in April. “But nobody feels sorry for me.”

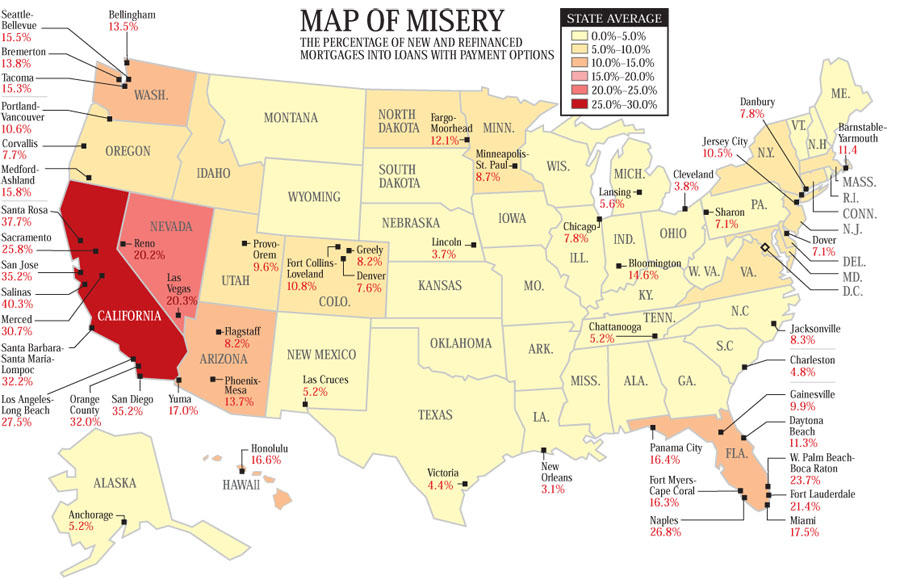

While the map of misery shows a percentage of toxic loans of roughly 15%, I wonder how many of these loans were written in just the last year or so?

Where will future “buyers” get the money for even a 5% down payment. If there are less buyers, what will that do for Seattle home values?

Now that we’ve seen one homedebtor facing foreclosure story here in Seattle, I wonder how many other stories are out there?

(Lynda V. Mapes, Seattle Times, 05-07-2007)