Last Friday, the Seattle Times ran an interesting story about a “limousine driver, earning little more than minimum wage” being approved for a loan on a $1.5 million condo in Bellevue Towers. The story was also picked up by at least one of the local television news outlets, and has been making the rounds on the internet all weekend.

Here’s a brief excerpt from the piece, titled $1.5M condo on $20K income? Prospective buyers lose $175K in Bellevue.

When Uzbek hot-dog vendor Danil Kasimov thought of America, he thought of the place portrayed in movies — a Land of Plenty where anyone’s dreams could come true.

In 2000, he emigrated to the U.S., settled in Redmond and became a limousine driver, earning little more than minimum wage.

Two years ago, a real-estate agent suggested he consider purchasing a condominium at the luxurious Bellevue Towers. To Kasimov, it seemed his vision of America was unfolding with the ease of the touch-screen showing eventual views from his dream condo on the 32nd floor.

Delighted that he prequalified for a $1.5 million condo on his $20,000-a-year income, he put down more than $75,000 in earnest money he borrowed from a friend.

But that money — and nearly $100,000 from five other prospective condo buyers — soon evaporated. The six filed a lawsuit in King County Superior Court this week against Bellevue Towers and JP Morgan Chase Bank, alleging the lender falsified documents, making it possible for them to prequalify for loans they could never actually get.

Now, before I get into the numerous problems with this article, I want to say up front that I’m not attempting to stick up for the banks, the real estate agent, or anyone else. Far from it. My purpose here is merely to point out the incredible one-sidedness and poor reporting in this Times article. I would also like to point out that most of these facts were brought to light by a number of commenters on the Seattle Times story, including “cocoas” and “Vesta.” I’m just highlighting these issues here because I think the full story should be heard.

All of the information in this post can be found in publicly-available records, accessible to anyone online in a matter of minutes. Links are provided for all sources.

Claim: Danil Kasimov is “a limousine driver, earning little more than minimum wage.”

Reality: Public records show a Danil Kasimov as the owner of a limousine company named Action Towncar.

A simple search of Washington State business licenses reveals that Mr. Kasimov is in fact the owner of Action Towncar, LLC, a Redmond-based limousine company, not merely a “limousine driver,” as stated in the article. Of course, this does not tell us how much Mr. Kasimov is earning, so it is possible that the “little more than minimum wage” part could be true.

Claim: Danil Kasimov was unwittingly duped by a real estate agent and a flashy sales presentation into signing paperwork he had no way of understanding.

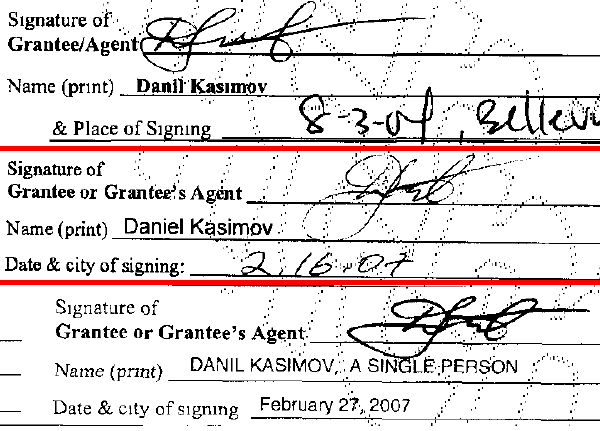

Reality: Public records show three different purchases of real estate in the Redmond/Bellevue area by a Danil Kasimov over the last five years, totaling nearly $1.6 million.

July 2004—Danil Kasimov purchases a condo for $240,000. February 2007—Danil Kasimov purchases a 4-bed, 1,800 sqft house for $665,000 and a 3-bed, 3,100 sqft house for $686,000. The address listed on two of the parcels matches the address for the Danil Kasimov that owns Action Towncar, and the signatures on the paperwork of all three home purchases match each other.

{kind=link}

Both of the $600k homes were foreclosed on in January of this year. Mr. Kasimov appears to still own the 2004 condo. Should Mr. Kasimov have been given any of these loans? It would appear not. However, it is also evident that Mr. Kasimov was not as naïve about the home buying and financing process as the article makes him out to be.

Claim: “…they were never given a copy of the contract — which was written in English, a language they didn’t understand…” and “Kasimov and the other plaintiffs, Yuri and Dora Aleksandrov and Davud Kasparov, none of whom are fluent in English…” (emphasis mine)

Reality: It is unlikely that any of these individuals are ignorant of the English language.

Danil Kasimov’s LinkedIn profile (the first result on a Google search for his name) reveals that he attended a school in his native Uzbekistan called the Uzbek State World Languages University, and according to the article, he has lived in the United States for nearly 10 years. Davud Kasparov attended the UW school of engineering and is now employed at a local aircraft engineering firm. Yuri & Dora Alexsandrov purchased a $336k home in 2001 which was refinanced six times between 2002 and 2008. None of these people are likely to be the confused and helpless foreigners that the article portrays them as.

I will point out that it is possible that there is another Danil Kasimov unrelated to the individual in the Seattle Times story, who just happens to own a limo company in Redmond and have a penchant for dabbling in real estate with dangerous loans. Possible, but highly unlikely, in my opinion.

The story printed in the Seattle Times portrays a starry-eyed, helpless group of individuals that were taken advantage of by a slimy real estate agent (who is inexplicably not named by the Times), shady lenders, and overzealous salespeople. The “angle” on the Times story is clear: Danil Kasimov and the others listed in the suit against Bellevue Towers are unwitting victims. It would appear that Nancy Bartley, the author of this article, had a story in mind that she wanted to tell, and did not bother to even spend 30 minutes researching the supposed victims online and in public records.

Danil Kasimov and the others involved in the lawsuit against Bellevue Towers may have a valid legal case, or they may not. But when we are given a more complete picture of the individuals involved in this story, it becomes clear that it is not as cut and dry as the Seattle Times has made it out to be. In reality, it would appear that everyone in this story likely attempted to victimize everyone else, and in the end, they all lost.

Update 02/25: The Seattle Times has corrected some of the errors and omissions in the article. See below for details.