The Seattle Times ran a story on Saturday that is worth it’s own post here. While the narrative consists mostly of the usual “personal interest” angle stuff (single mom finds her fourth home in foreclosure when she loses her $800,000 per year job as a mortgage executive, etc.), the attached Tableau interactive tells a much more interesting story:

Home values in King County grew nearly three times faster than household income from 2000 to 2008, with barely a lull after the dot-com bust at the beginning of the decade.

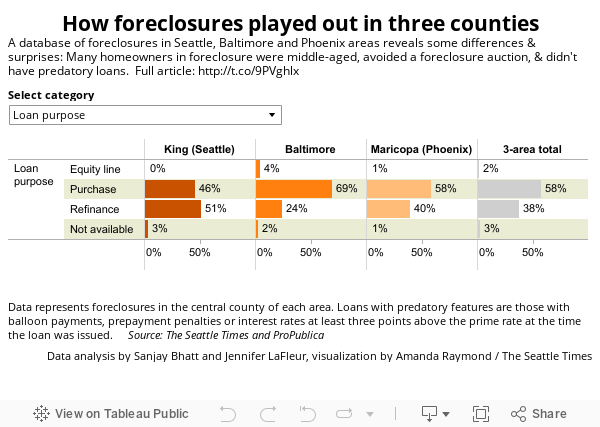

About 40 percent of homeowners in the Seattle-area foreclosure data had owned their houses for more than five years. One out of five had owned for a decade or longer — long enough to build up substantial equity.

That may help to explain one defining aspect of the Seattle-area foreclosures: About half involved refinancing, the data show, a much higher rate than in the Phoenix or Baltimore areas.

The most common loan? A hybrid adjustable-rate mortgage that resets to higher payments after two years, a product that encouraged repeat refinancing.

Some homeowners cashed out equity to pay debt, make home improvements or finance a business. Homeowners also lost equity as refinancing added loan fees.

I assume they selected Baltimore as a comparison because it’s fairly close to Seattle in population, geographic size, and density. Phoenix was of course the “extreme” comparison point.

Although their analysis was only based on a sample of 400 foreclosures per market, this data does explain why it is so ridiculously easy to find outrageous examples of equity withdrawl gone wild.

Lili Sotelo, managing attorney at Northwest Justice Project, said she’s seen thousands of homeowners who got caught up in the refinancing frenzy.

“[Borrowers] thought they had to get on the equity train,” she said. “No one thought the train was going to crash.”