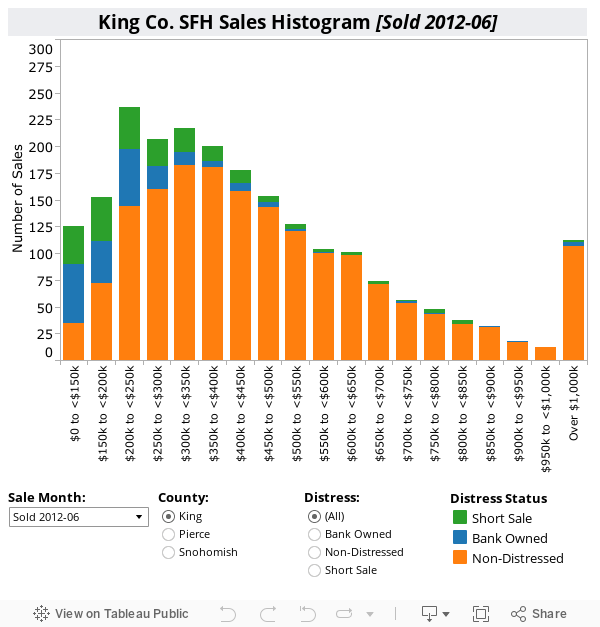

I thought it might be interesting to re-visit the sales histogram chart that I first published a few times last year.

To generate the chart below, I took all the sales data for single-family homes sold in King, Snohomish, and Pierce Counties from the beginning of 2010 through the end of March. Since my data download puts late-reported sales into the month that the sale actually took place rather than in the month they were reported, there is a slight difference in the number of sales I’m counting vs. what the NWMLS reports each month.

By default the chart shows just King County sales in March. Use the controls below to view different months, or to see what the mix looks like for Snohomish or Pierce County. I’ve also added color-coding and controls to separate out “non-distressed” sales from the sales of bank-owned homes and short sales.

Now that I’ve been downloading the sales data for over a year, you can flip back and forth between the latest January, February, and March and the same month a year ago. It’s interesting to see that although the median price has only fallen $25,000 between March 2010 and March 2011, the concentration of sales in the lower prices seems to have shifted noticably to the cheaper brackets.

It’s also interesting that although the median has fallen $25,000, the bin with the most sales (the approximate mode) has been relatively steady, holding in the $250k to <$300k range for ten of the last fifteen months. In Snohomish County the trend is even more pronounced, with the median having given up $21,500 between January 2010 and March 2011, but the mode holding steady in the $200k to <$250k bin for all but three of those months.

Overall it seems that movement on the low end is picking up pretty strongly in 2011. With banks seemingly processing more foreclosures and getting them onto the market more quickly, it would appear that some serious market clearing has finally begun. Of course, just as we’re really getting the market rolling on a true path to correction, the Washington State legislature has decided to step in again and slow things down with another bill to slow the foreclosure process. But that’s a topic for another post.