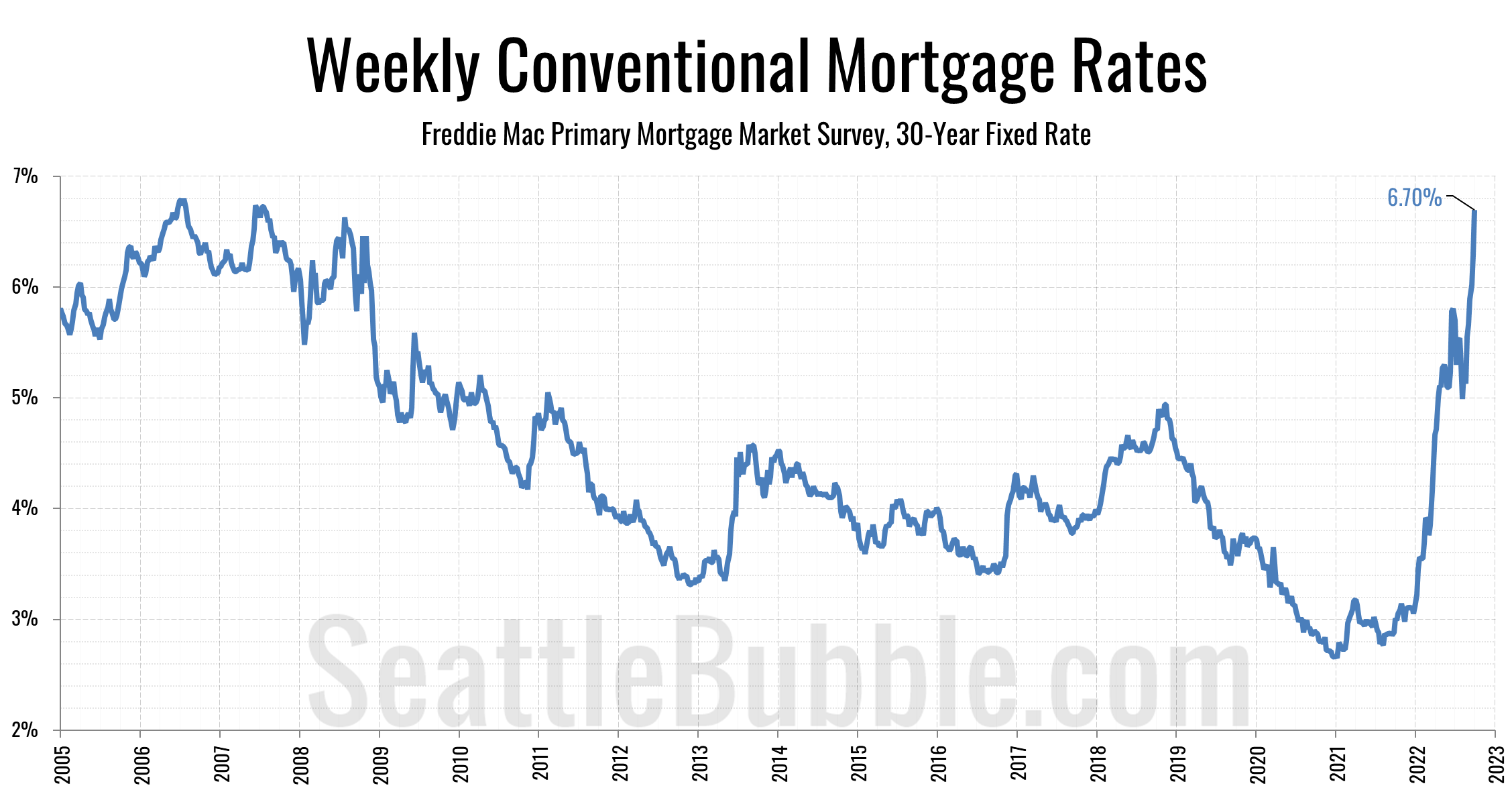

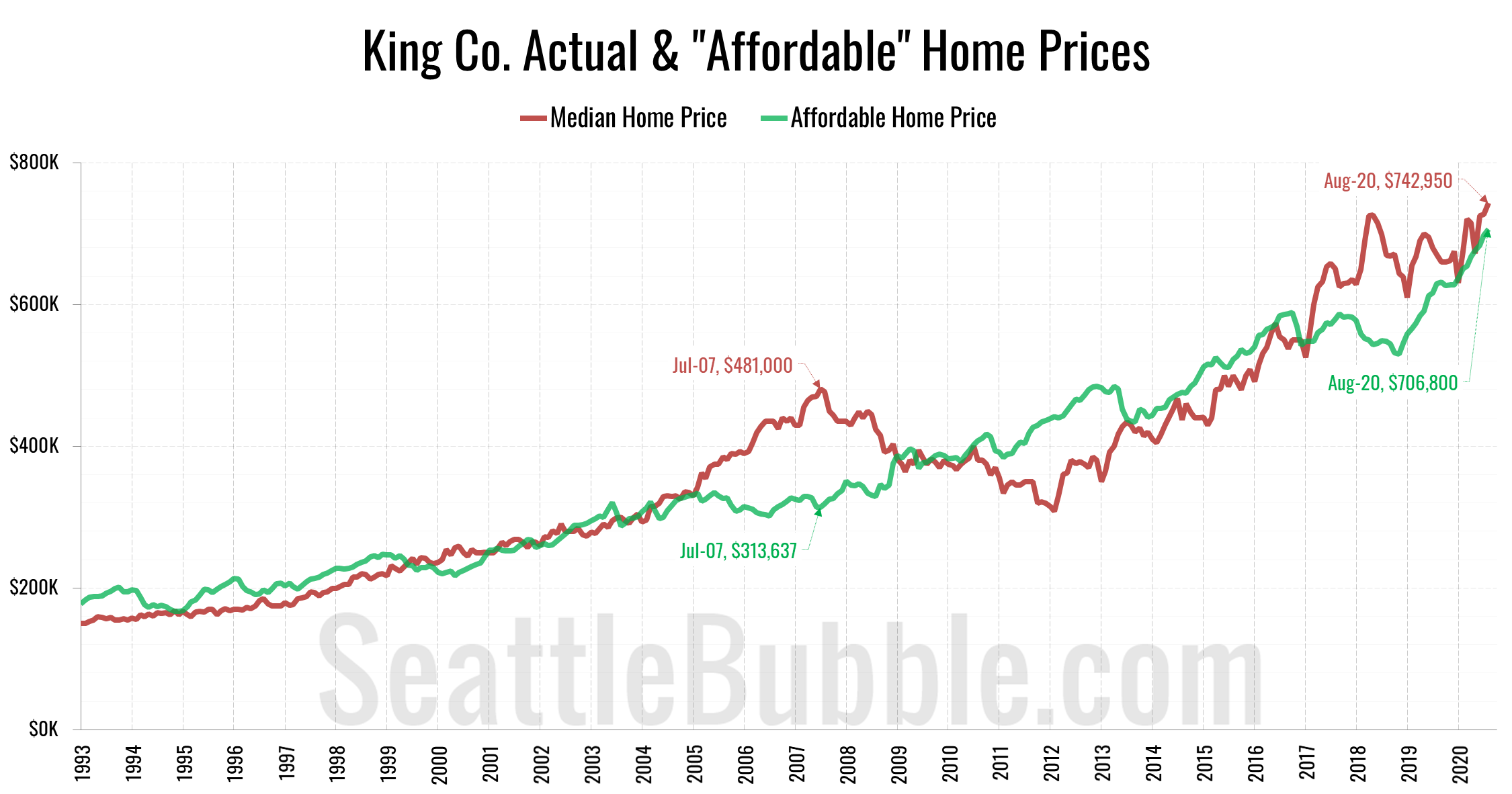

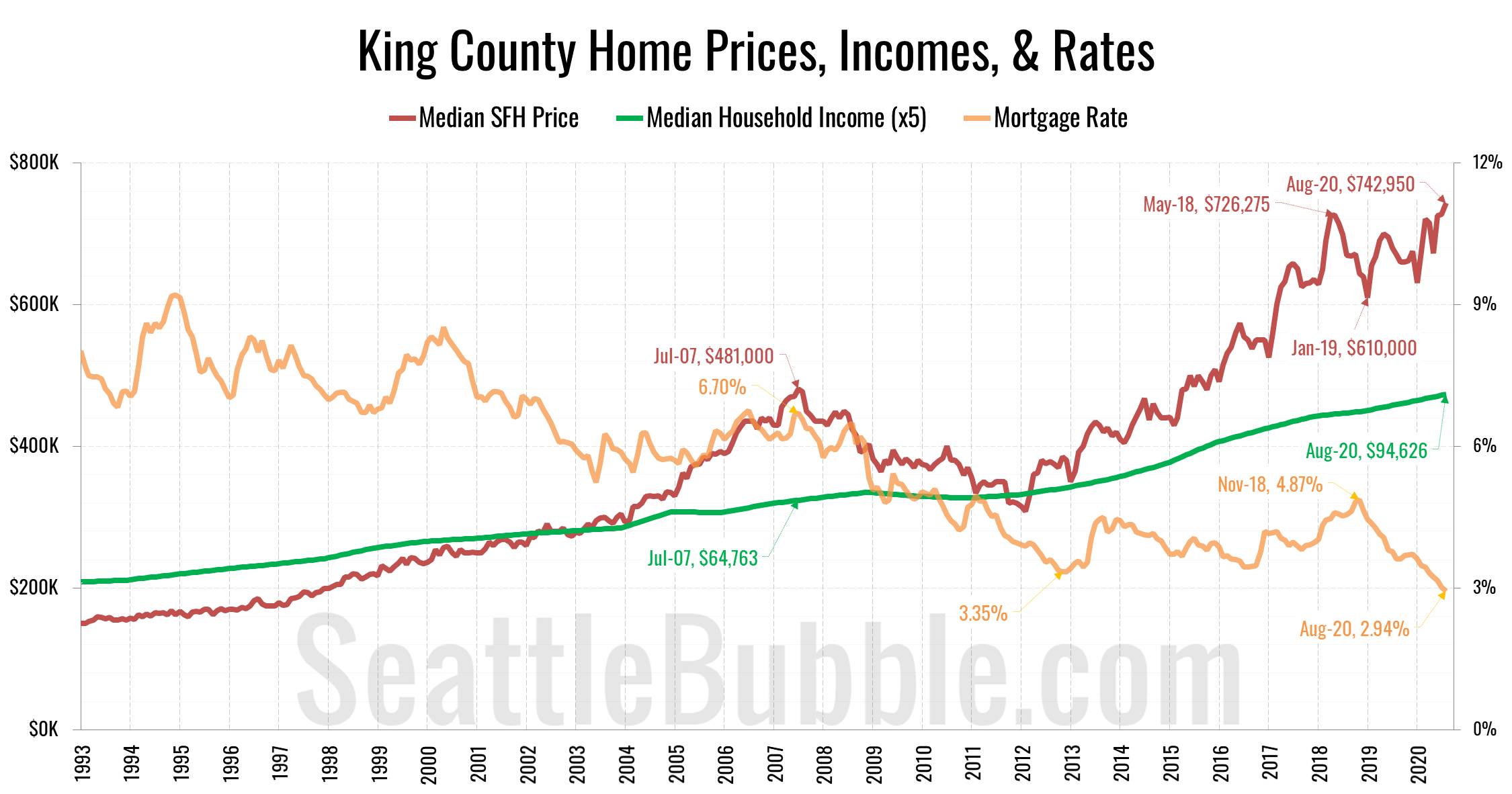

As of February, the monthly payment for the median-price single-family home sold in King County at current mortgage rates was $3,945. The good news: This is down from an eye-watering $4,758 in October. The bad news: It’s up dramatically from just a year prior, and 59% higher than what we saw at the peak of the previous housing bubble…