I like to keep tabs on what’s going on in my neighborhood, and when a little house a block away was listed for rent on Craigslist (screenshot) this week, I remembered seeing it as a foreclosure on the market for sale last year. I got a little curious to know some more about this home’s…

Tag: mortgages

Are Obama & Romney Avoiding Housing to Avoid Talking About Killing the Mortgage Interest Deduction?

There is one major political topic that has been mysteriously absent from both major presidential campaigns during this year’s presidential election season… housing. Nick Timiraos noted this in the Wall Street Journal in early September. Here we are in late October, four debates later, and nothing has really changed. Barely a peep about housing from…

Reader Question: What’s the Deal With HARP 2.0?

I received the following email from a reader asking about the federal government’s Home Affordable Refinance Program (HARP) earlier this week: I have been looking into the HARP 2.0 program to refinance my home. I qualify according to program guidelines, but find it hard to shop interest rates and find lenders that deal honestly with…

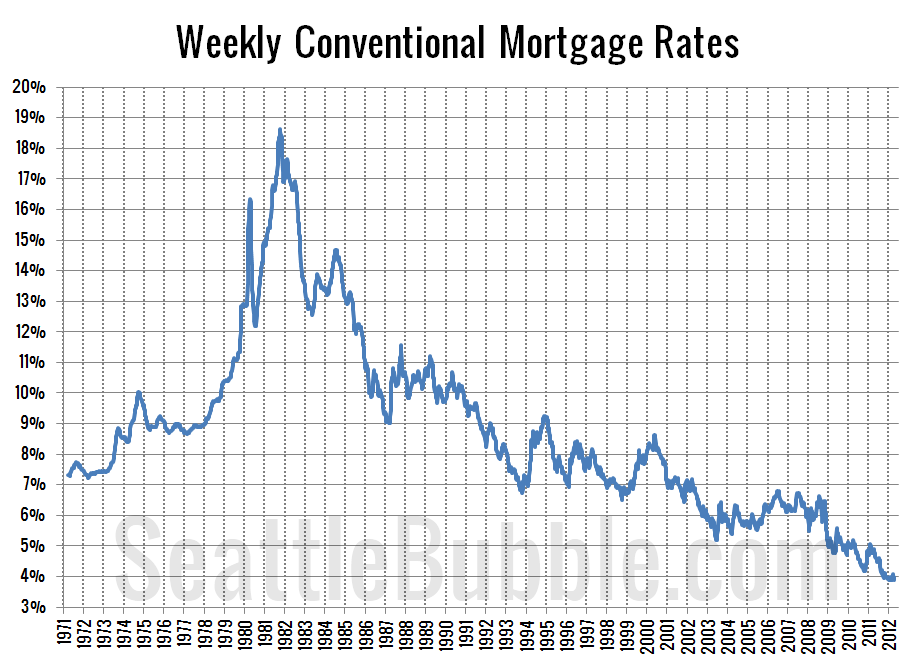

Will Higher Interest Rates Kill the Housing Market?

Here’s a sampling of quotes from news articles about mortgage interest rates. “…a new reality: The economy has made the transition from tentative to robust recovery, and the period of historically low interest rates is ending.” “In the residential market, the belief that the period of historically low interest rates may end has begun to…

Running the Numbers on the Flat Homeowner Deduction

[Read Part 1: Proposal: Replace the Mortgage Interest Deduction with a Flat Homeowner Deduction] In the comments on the proposal I made yesterday, Doug asked a reasonable question: Have you figured out what the deduction would be if you did this, and made it deficit neutral? That would be an interesting exercise. Good question. Let’s…