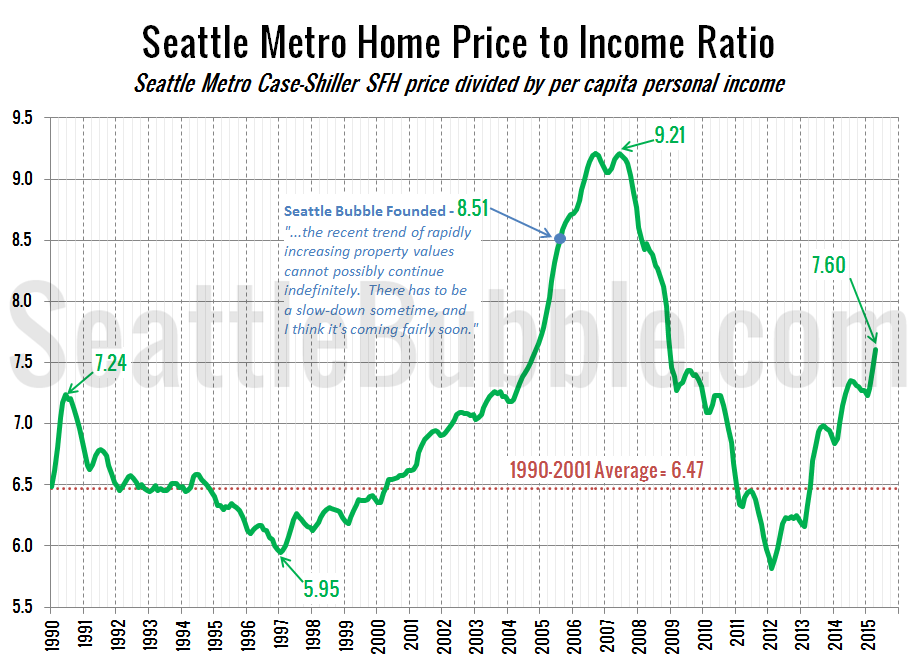

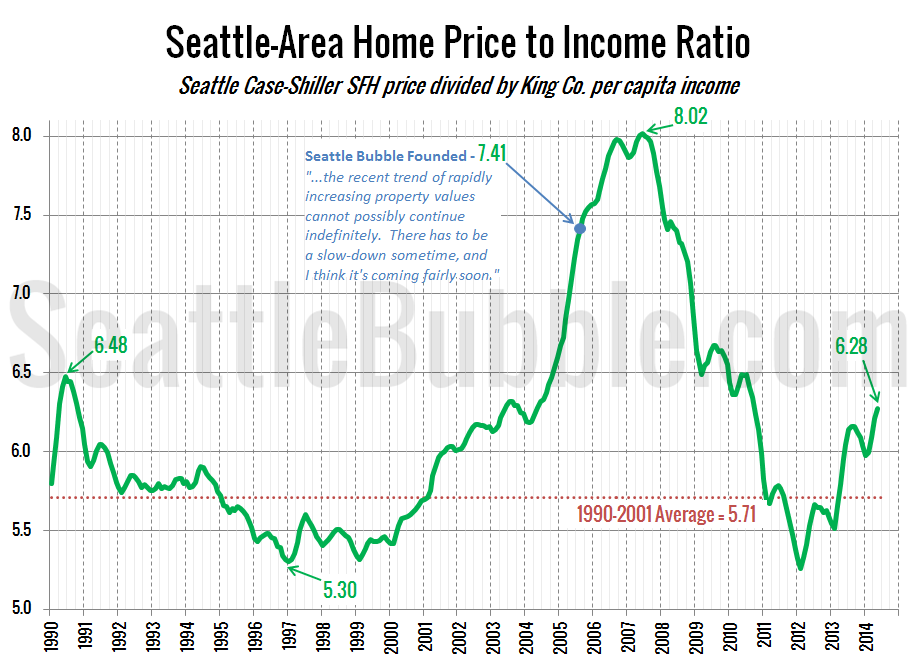

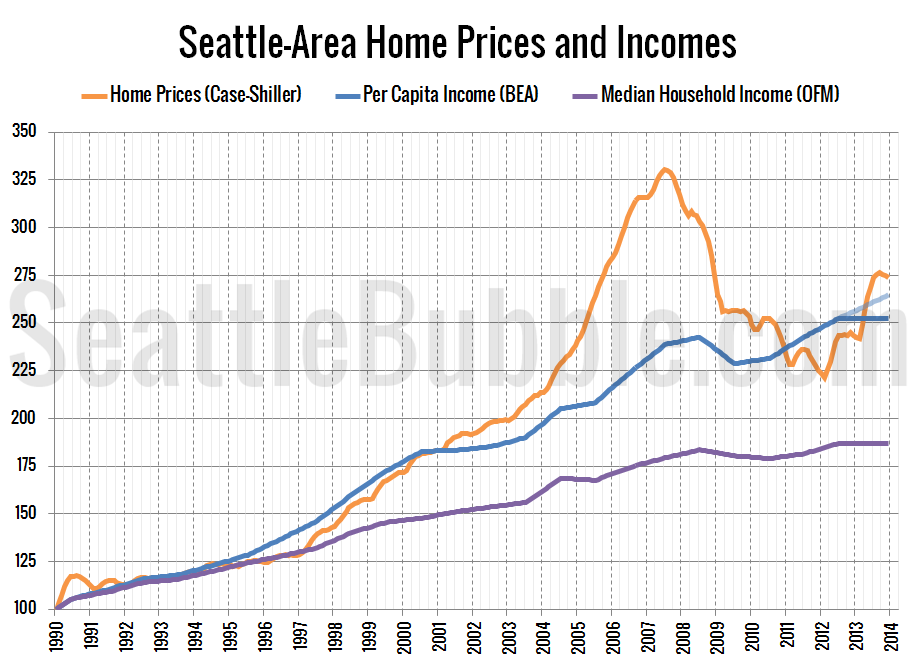

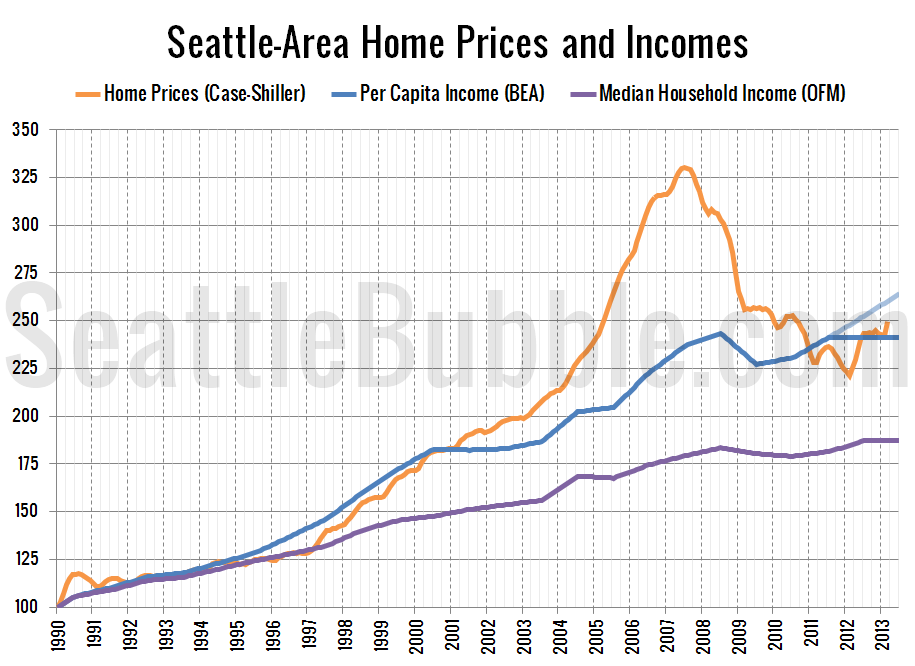

It has been a while since we last looked at one of our primary housing bubble metrics: local home prices compared to incomes. In the next chart I am using the Case-Shiller Home Price Index for the Seattle area (which rolls together King, Snohomish, and Pierce counties) and Bureau of Economic Analysis data on per…