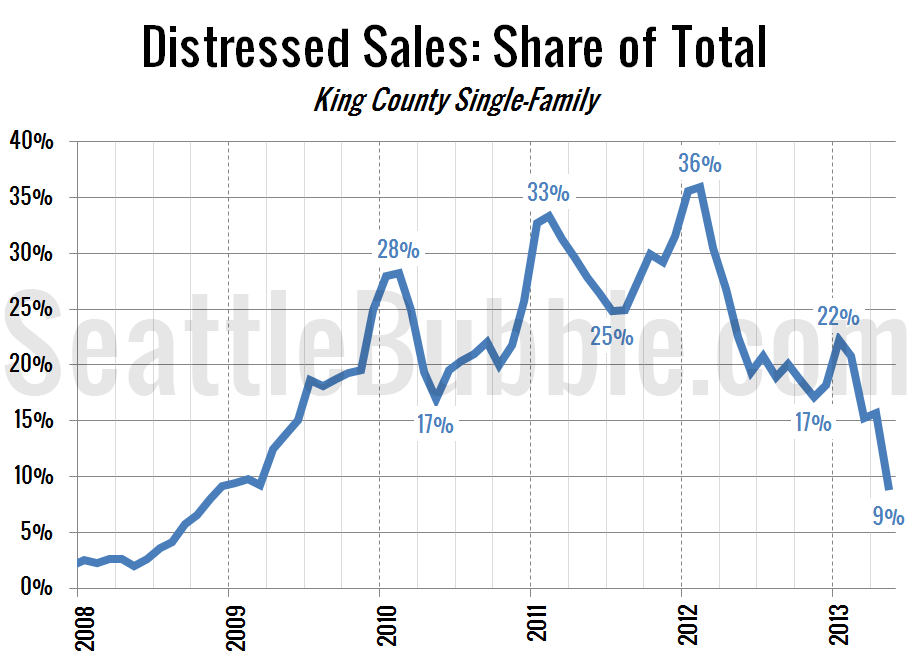

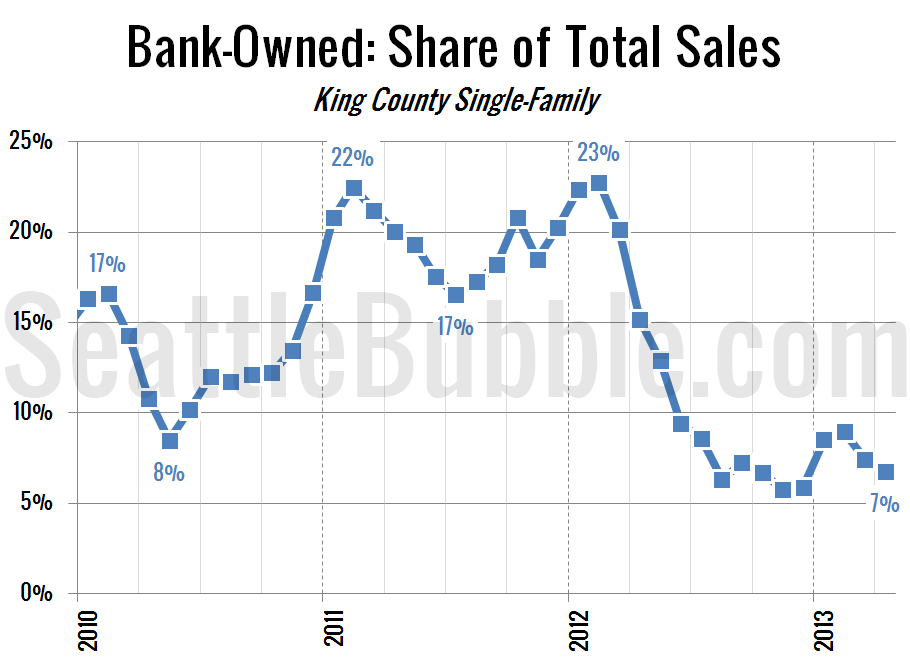

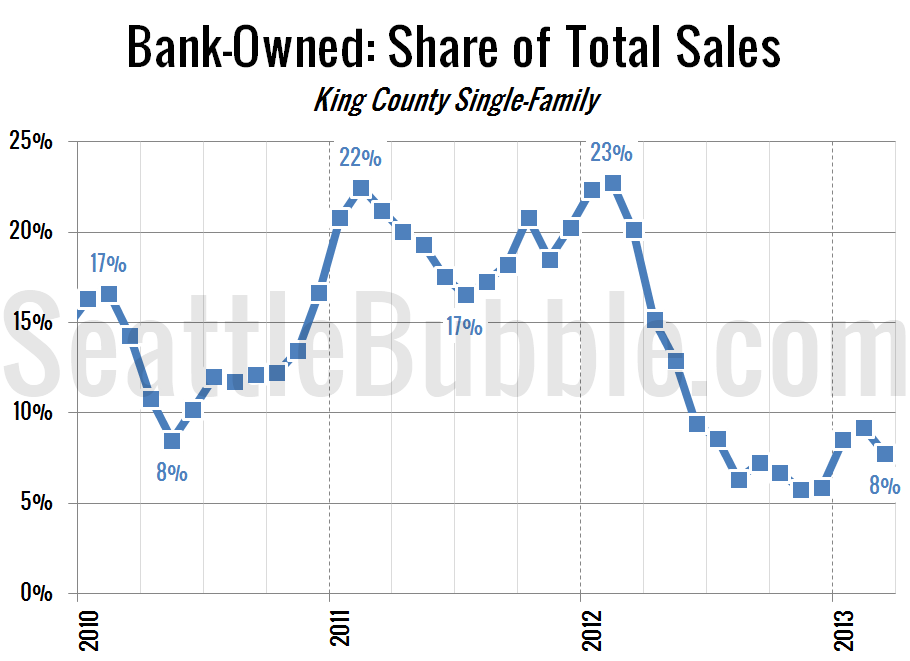

Time to take look at what share of the monthly sales are being distressed sales—bank-owned and short sales. In June 2012 9.4% of the sales of single-family homes in King County were bank-owned. In June 2013 that number was just 5.7%. We’ve now matched the low of 5.7% set in November. Short sales bounched back…