An article in today’s Seattle Times goes nicely with Mr. Cohen’s article in the P-I a couple days ago.

More sellers are growing desperate as homebuying stalls locally

I especially like the first part of the subtitle text (emphasis mine):

The Puget Sound area housing market, supposedly immune to the forces pulling down others across the country, is seeing more inventory, fewer sales and falling prices, and that’s stressing out Seattle-area sellers — particularly those who need to sell quickly to avert foreclosure or move out of town. Instead of taking advantage, buyers are sitting on the sidelines.

Guess who didn’t write this article. If you guessed Elizabeth Rhodes, #1 Local Housing Cheerleader, you win. Anyway, here are some interesting excerpts:

The Seattle-area housing market, once touted as bulletproof against the forces that were pulling down other markets across the country, is now stressing out sellers, who are seeing inventories rise, sales fall and prices drop. Many are shellshocked — particularly those needing to move out of town or trying to forestall foreclosure.

I wonder why they would be “shellshocked.” Maybe because this very paper was loudly proclaiming Seattle’s immunity to the housing bust to anyone who would listen? Anybody remember this gem from a big front page story in the Times back in September 2006?

Princeton economist Paul Krugman, writing in The New York Times, said: “The long-feared housing bust has arrived.”

Nationally speaking, anyway.

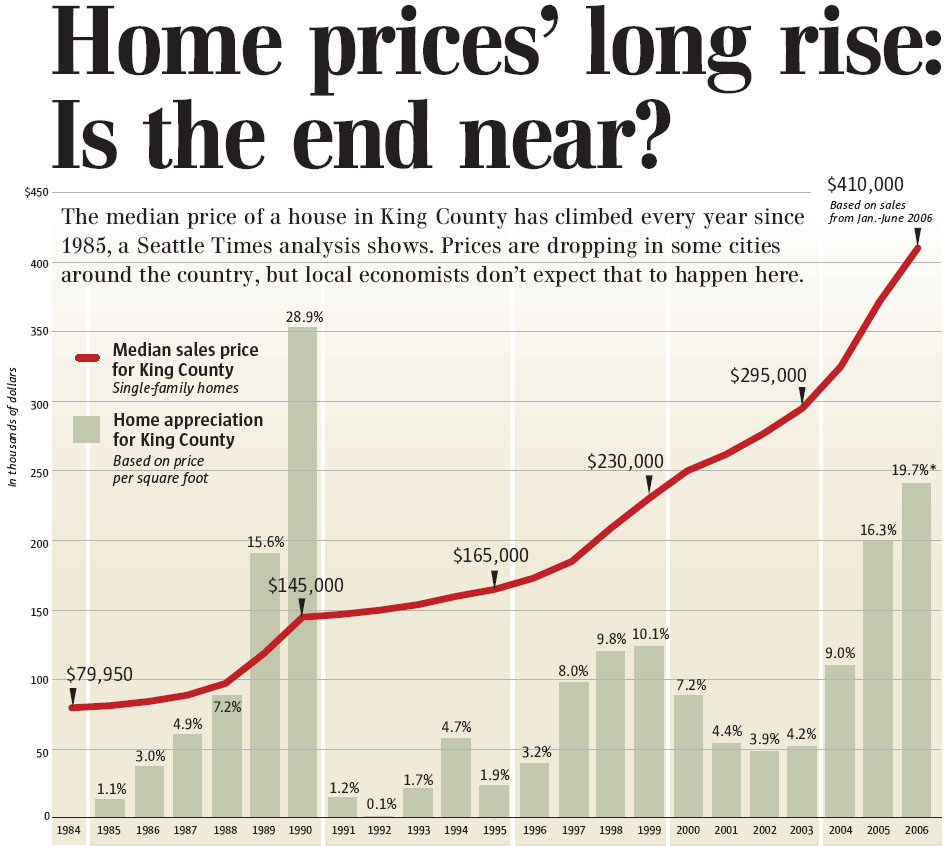

If history is any indication, King County may escape it, according to a Seattle Times analysis of single-family-home prices. It shows that appreciation rates have risen and fallen, sometimes precipitously.

But not once since 1985 — through recession years, interest-rate spikes, wars and employment downturns — has the countywide median price of a single-family home fallen, although it’s come close.

Also note the subtitle on the graphic:

{kind=link}

Prices are dropping in some cities around the country, but local economists don’t expect that to happen here.

Anyway, back to today’s article:

As recently as last year, buyers were paying above list price and sometimes even waiving home inspections to come out the winner in multiple-offer situations. Now they seem content to wait for … what exactly? Prices to drop even further? Superior mortgages? Clarification of the Wall Street crisis? The election?

Don’t you just love the condescending, almost mocking tone?

As the asking price on their Shorewood house keeps falling, the financial and emotional burdens keep mounting for Dave and Kim Mantel, who take ownership next month of a new house in Tucson, where they plan to retire.

“When we made our decision last December to go ahead and start the Tucson construction, we couldn’t have envisioned having this much trouble selling our house,” Dave Mantel said. “We knew the nationwide market was having trouble but Seattle seemed immune. We just couldn’t have picked much worse timing.”

The house in Shorewood, which is between West Seattle and Burien, has a panoramic view of Puget Sound and the Olympics. The Mantels put it on the market in April after a remodel. They’ve lowered the asking price four times — the last a $50,000 drop to $799,000 — but have yet to receive a firm offer.

On the one hand, I feel bad for people like this family that bought the line they were being fed by the likes of the Times and other rosy news outlets. On the other hand, when you’re spending close to a million dollars on something, you have at least a little responsibility to do some due diligence. Folks like this family and others that “need to sell” that bought into the hype are getting burned if they overpaid for their homes. I guess I’d have more sympathy if nobody saw the present situation coming, and today’s market came out of left field totally unexpected.

(Stuart Eskenazi, Seattle Times, 10.02.2008)