Let’s have a look at the latest data from the Case-Shiller Home Price Index. According to January data that was released today, Seattle-area home prices were:

Up 0.2 percent December to January

Up 10.7 percent YOY.

Down 2.8 percent from the July 2007 peak

Over the same period in 2014-2015 prices were down 0.5 percent month-over-month and year-over-year prices were up 6.8 percent.

The Seattle area’s month-over-month home price change was positive again in January. Unlike the last few years, home prices did not dip the last few months of the year, but instead the gains just slowed down. This is similar to what happened in 2005 and 2006, although the affect was even stronger then. Meanwhile, the year-over-year price change in January jumped back up into double digits for the first time since April 2014, as well.

In summary: It is still a terrible market to be a home buyer in.

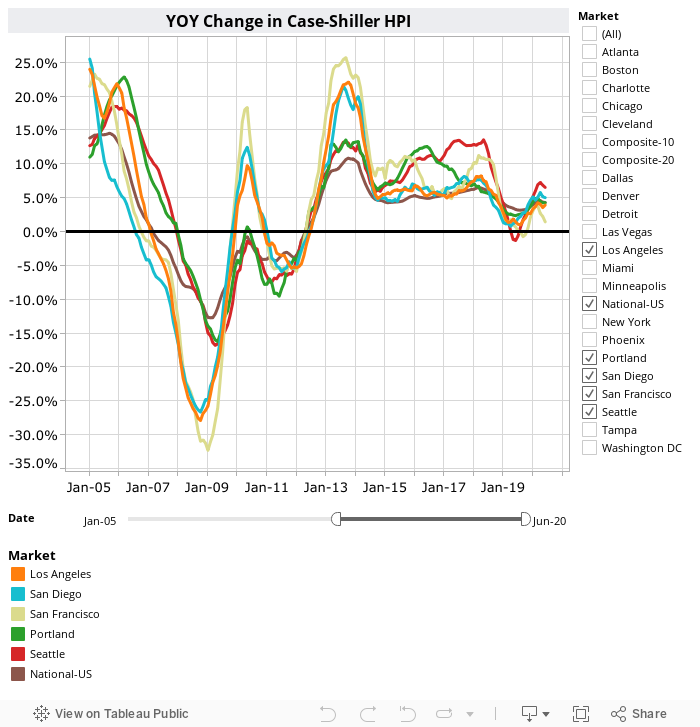

Here’s a Tableau Public interactive graph of the year-over-year change for all twenty Case-Shiller-tracked cities. Check and un-check the boxes on the right to modify which cities are showing:

Seattle’s rank for month-over-month changes was flat at #8 January.

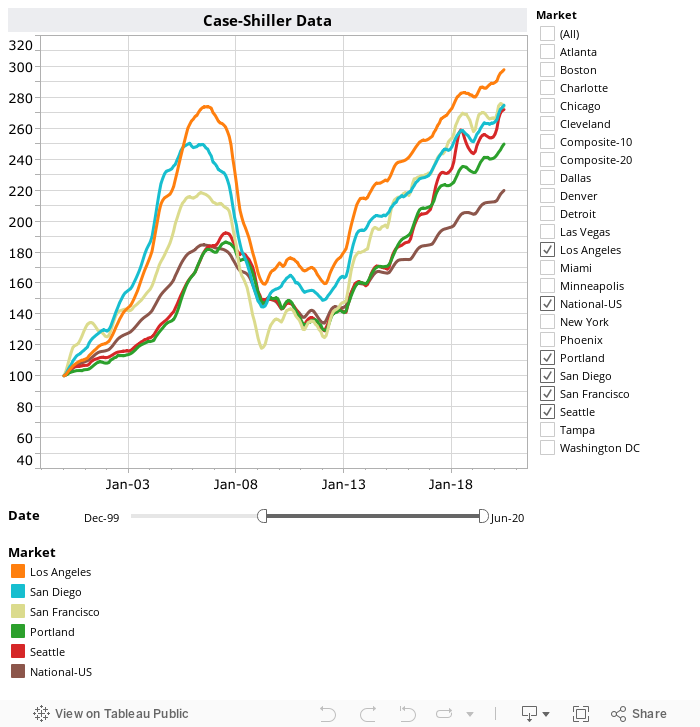

Hit the jump for the rest of our monthly Case-Shiller charts, including the interactive chart of raw index data for all 20 cities.

In January, just one of the twenty Case-Shiller-tracked cities gained more year-over-year than Seattle (two fewer than in December):

- Portland at +11.8%

Clearly Washington and Oregon have an economy that is literally the envy of other states.

Denver, Portland, and Dallas both hit new all-time highs in January.

Eighteen cities gained less than Seattle as of January: San Francisco, Denver, Dallas, Tampa, Detroit, Los Angeles, San Diego, Miami, Phoenix, Las Vegas, Atlanta, Charlotte, Minneapolis, Boston, Cleveland, New York, Washington, and Chicago.

Here’s the interactive chart of the raw HPI for all twenty cities through January.

Here’s an update to the peak-decline graph, inspired by a graph created by reader CrystalBall. This chart takes the twelve cities whose peak index was greater than 175, and tracks how far they have fallen so far from their peak. The horizontal axis shows the total number of months since each individual city peaked.

In the 102 months since the price peak in Seattle prices are down 2.8 percent.

Lastly, let’s see what month in the past Seattle’s current prices most compare to. As of January 2016, Seattle prices are still approximately where they were in March 2007.

Check back tomorrow for our monthly look at Case-Shiller data for Seattle’s price tiers.

(Home Price Indices, Standard & Poor’s, 2016-03-28)