KUOW ran a story a couple days ago that I would like to address here: Thousands Of Foreclosures Sit Off Market In Seattle Area

The Seattle-area housing market could use an injection of inventory. It’s on a tear right now, fueled by high demand and low supply, and hooked on low-interest rates.

And there is a potential supply of lower-priced homes in the region. Those are the 4,300 foreclosed homes from Everett to Tacoma that are now owned by banks, according to RealtyTrac.

More than 4,000 houses added to the market would be a rush – that would be two-thirds of what the region sells in a single month.

But these houses are just sitting around.

There are a few big problems with this piece.

Problem 1: RealtyTrac data is misleading

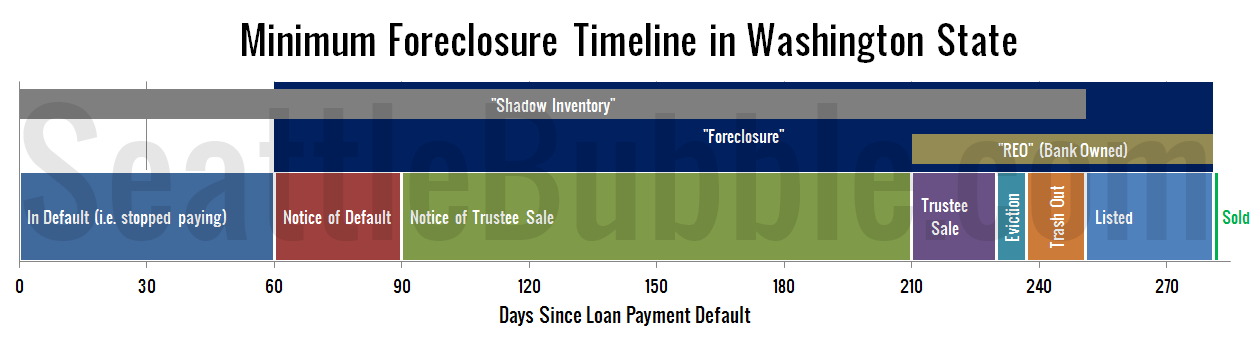

KUOW’s report is based on data from RealtyTrac, and RealtyTrac overcounts foreclosures. When most people think of a “foreclosed home” they are usually talking about a home that has actually been repossessed by the bank and sits empty (i.e. a bank owned home). When RealtyTrac gives data on foreclosure counts, they’re giving a total number of homes that are in “some stage of foreclosure (default, auction or bank owned).”

Here in Washington State, there is no public notice of default, so RealtyTrac’s numbers only count “auction” (i.e. homes that are scheduled for a bank auction according to the publicly-filed Notice of Trustee Sale) and “bank owned” (i.e. homes that have actually been repossessed by the bank via a Trustee Deed). If you look at the Washington State foreclosure timeline, you’ll see that any given home progressing at the fastest possible rate through the foreclosure process is going to sit in one of those two states between day 90 and day 281. Therefore, RealtyTrac’s data is a snapshot of 191 days—over six months—of the foreclosure pipeline.

Any snapshot of the foreclosure pipeline at a given time that includes both homes that have received a notice of trustee sale and those that have actually been foreclosed will include the last four months’ worth of homes that received a notice of trustee sale and the last two months worth of trustee deeds. Running those numbers for King / Snohomish / Pierce gives us 3,087 notices of trustee sale March through June and 698 trustee deeds1 in May and June, for a total of 3,785 homes progressing normally through the foreclosure pipeline as of the end of June. Again, this number assumes every home is moving as quickly as possible through the pipeline, which we know is not true since there are many ways to delay and extend the foreclosure timeline.

In other words, 4,300 sounds about right for the number of homes progressing normally through the foreclosure pipeline right now. These homes are not “just sitting around,” as claimed by KUOW. In fact, more than 3,000 of them are not yet even bank owned, meaning they are likely still occupied by the delinquent borrowers.

Problem 2: 4,300 homes is a drop in the bucket

According to NWMLS data, there were 6,472 closed sales (SFH+condo) in King / Snohomish / Pierce in the month of June. At the end of the month there were 9,710 homes on the market. That gives us a mere 1.5 months of supply for the three-county metro area.

Even if we assume that the 4,300 homes cited by RealtyTrac are “just sitting around” (which they are not) and were able to be immediately added to the market, increasing inventory from 9,710 to 14,010 would result in an increase of just 0.7 months of supply. Granted, 2.2 months of supply is definitely better than 1.5, but keep in mind that six months of supply is considered a “balanced market” that favors neither buyers nor sellers. 2.2 months of supply is still deep in sellers’ market territory.

In order to bring the Seattle-area housing market back into balance at the current level of demand, an additional twenty-nine thousand homes would need to be listed for sale—nearly seven times the claimed 4,300 homes that are “just sitting around” (but aren’t really).

A Better Headline

Frankly, 4,300 homes in some stage of foreclosure in the Seattle metro area is not news. If KUOW really wanted to run a piece about it though, the headline should have been “Thousands Of Homes Progressing Normally Through The Foreclosure Process In Seattle Area”

Are there a few homes here and there sitting empty for longer than the typical foreclosure process for one reason or another? Sure. Is it “thousands of homes”? Nope, no way, not true, just no.

Update: See the response from RealtyTrac VP Daren Blomquist at comment #9 below, and my response to him at comment #20.

1I had to make a calculated guess at Snohomish deeds of trust since they lump all deeds together in their online records search