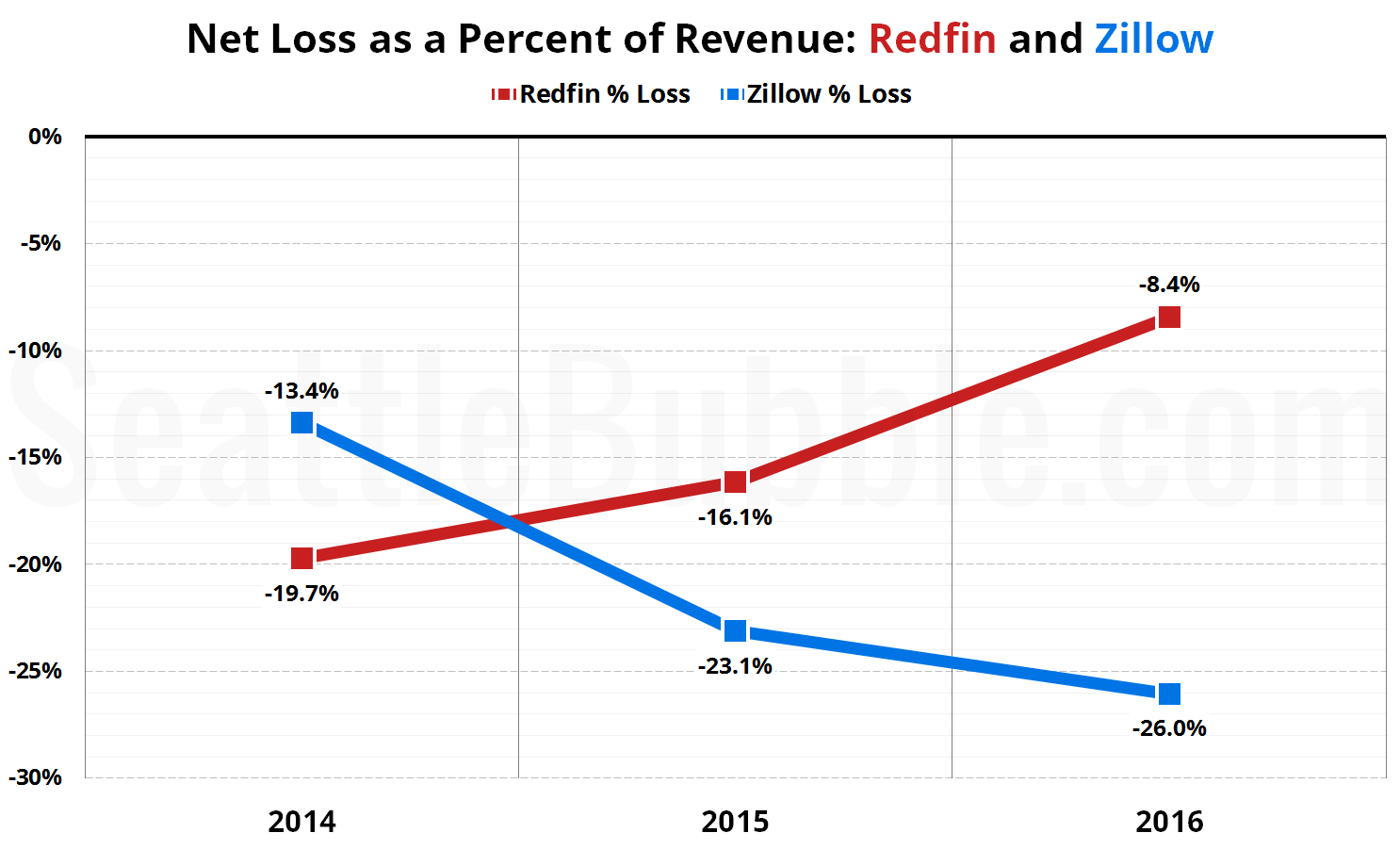

News broke late this afternoon that after 13 years as a “startup,” Redfin has finally filed their S-1 with the SEC, signalling their intent to make an initial public offering (IPO) later this year.

Let’s take this opportunity to directly compare some financial and usage data between Redfin and Zillow.