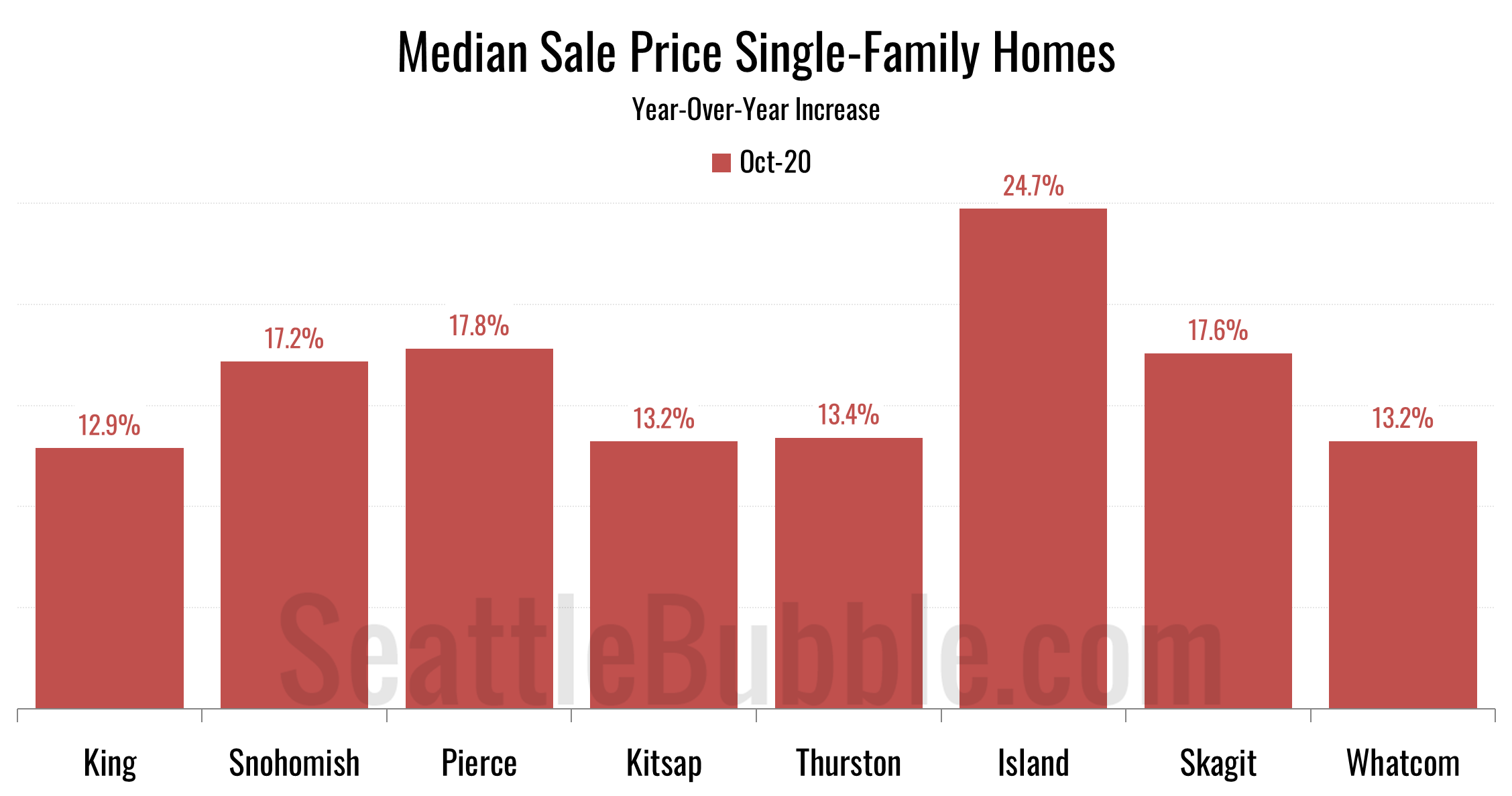

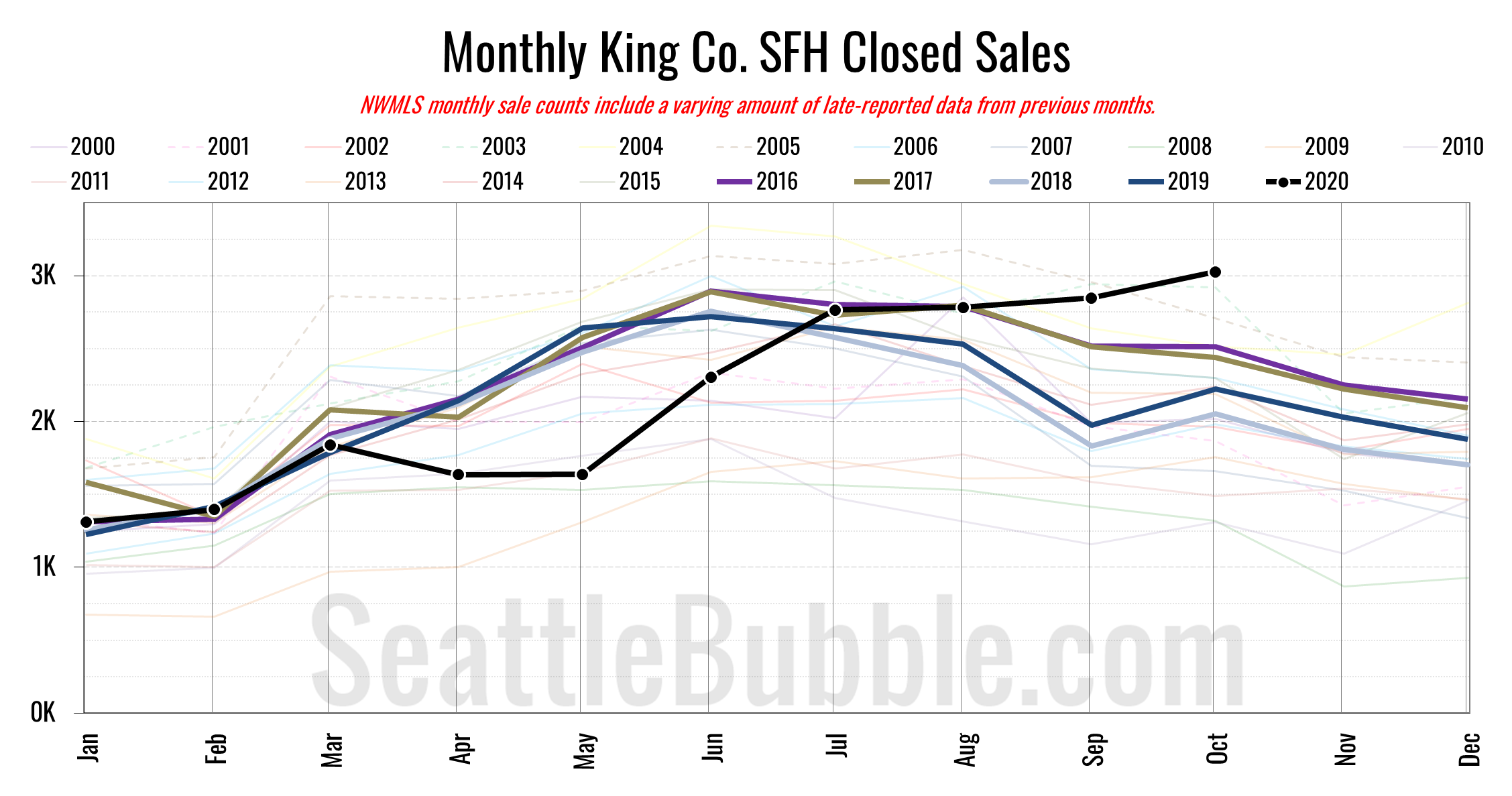

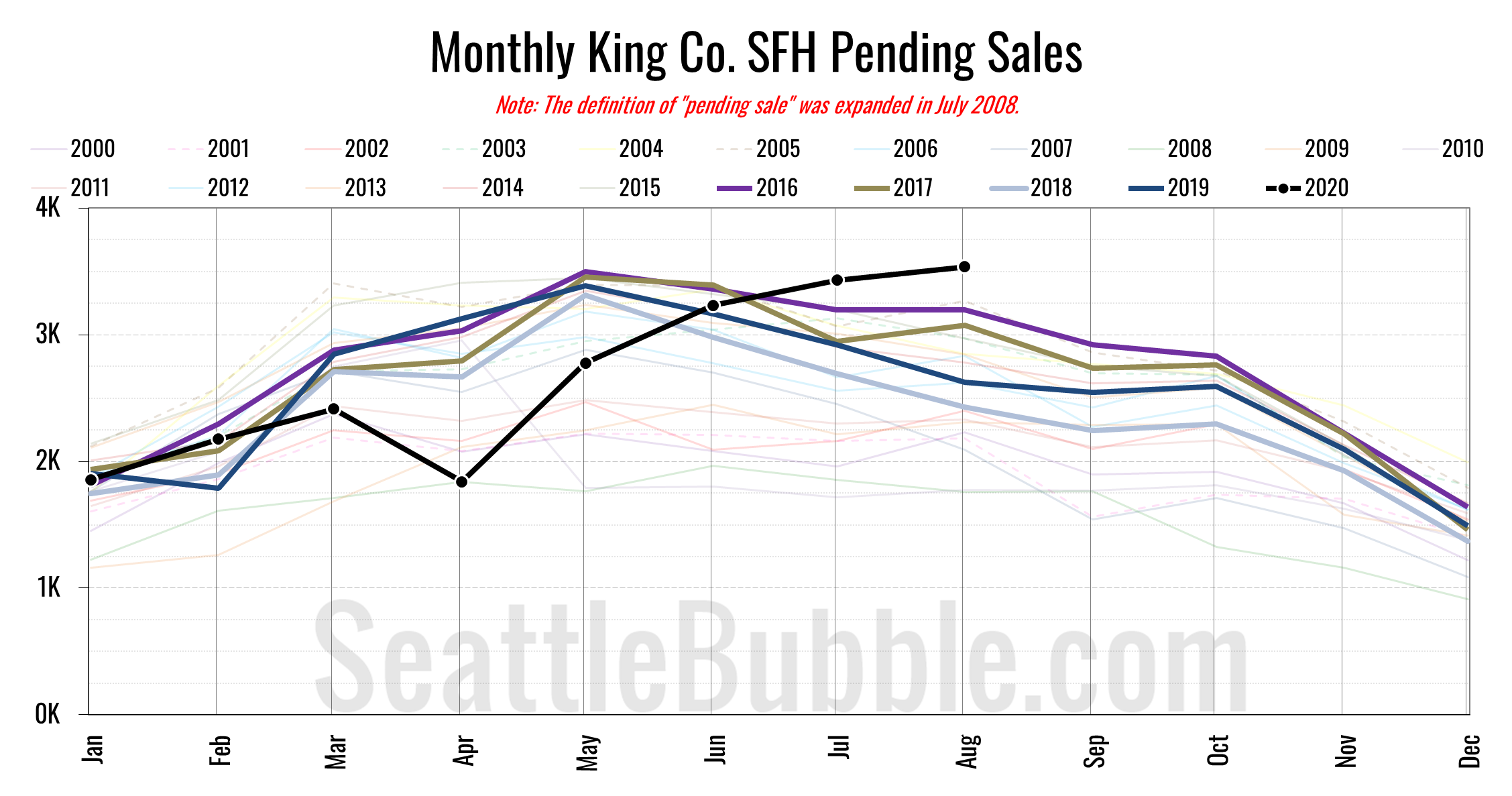

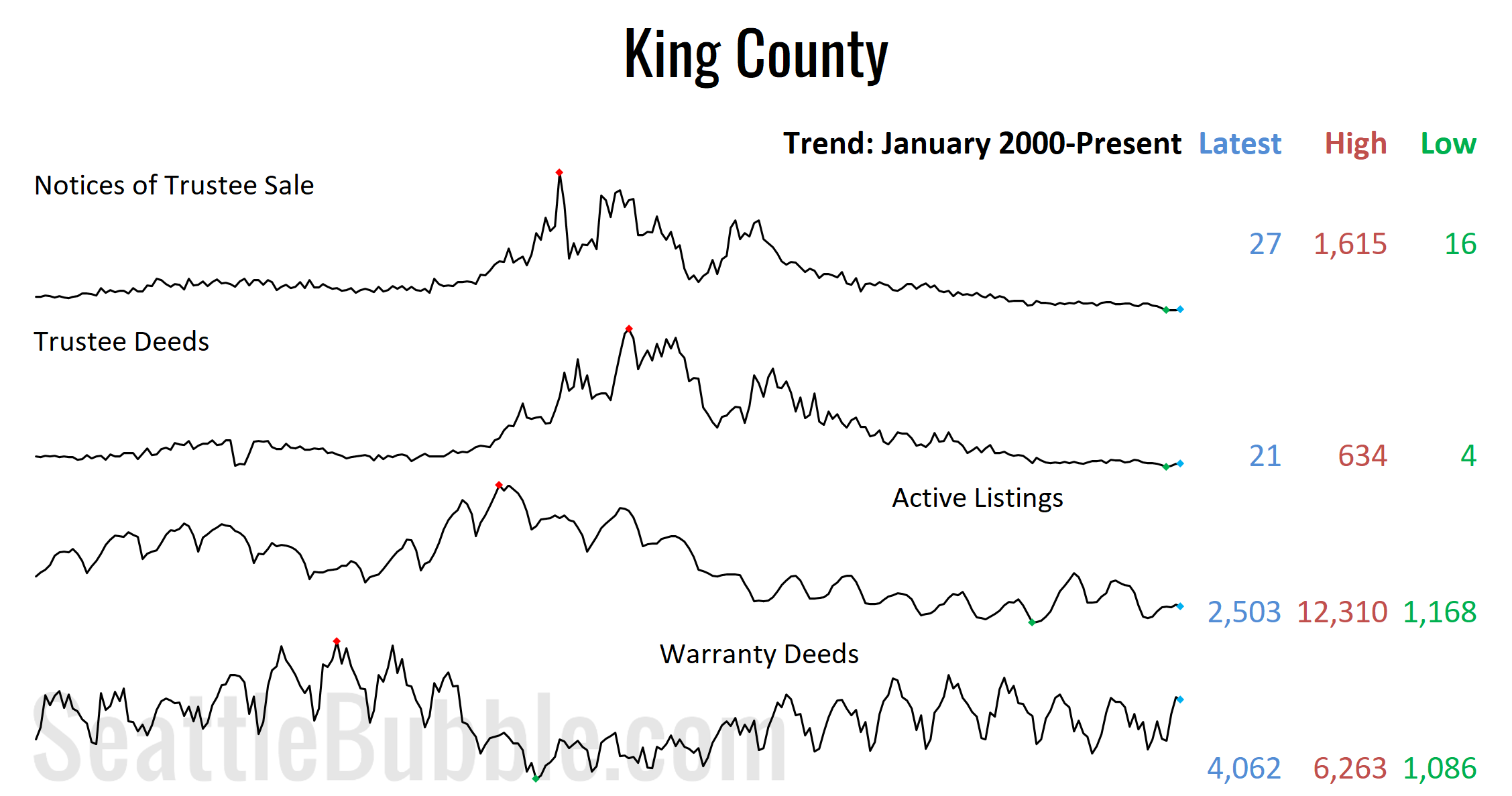

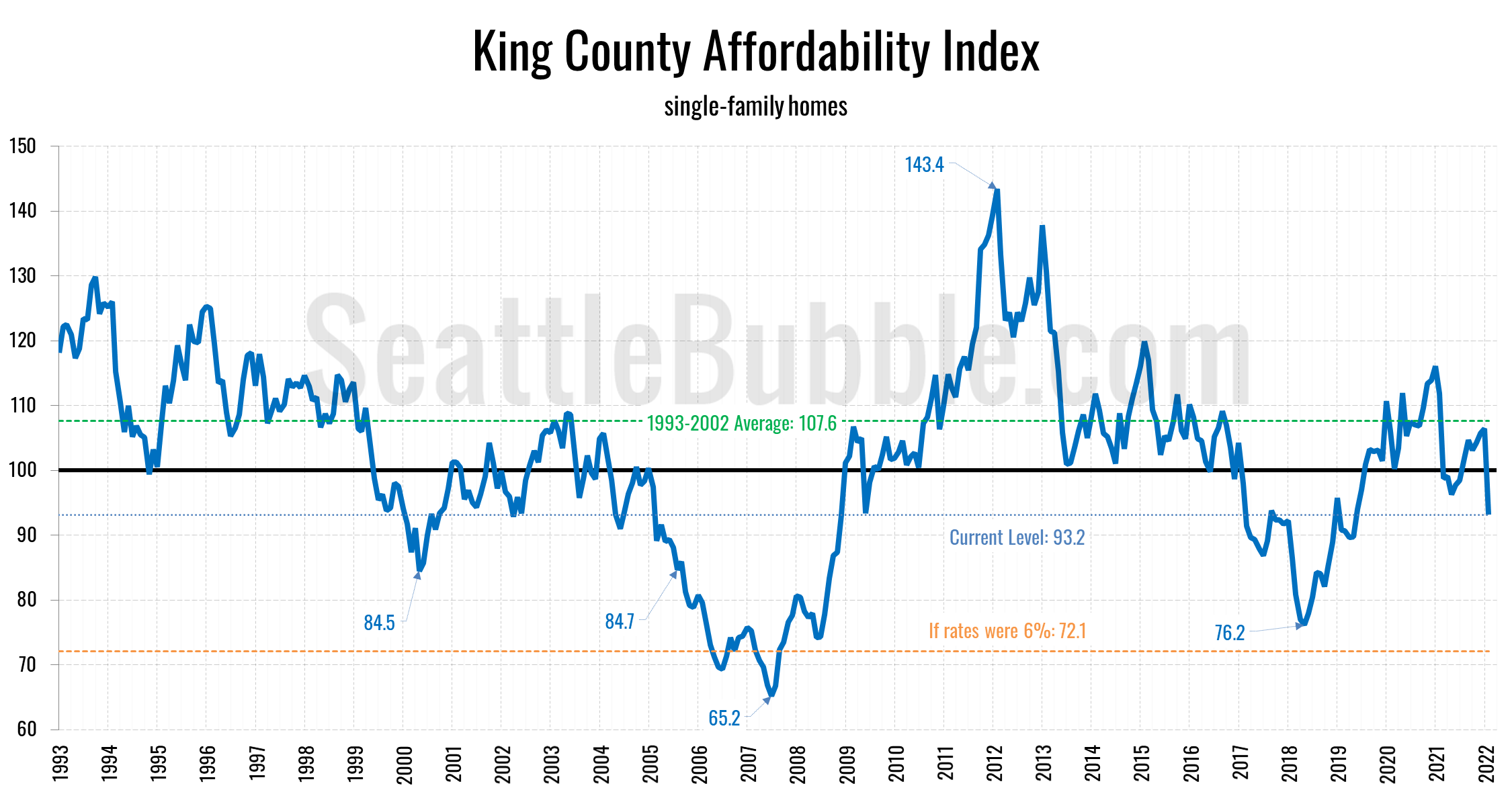

Since we’ve been gone for so long, I thought I’d start back up with somewhat of an overview post. Let’s just take a look at what’s going on in the Seattle-area (King County) housing market recently.

One of the biggest topics on everybody’s mind lately is home prices, so let’s start there…